Operations Manager Cover Letter Examples and Templates for 2024

- Cover Letter Examples

- How To Write a Operations Manager Cover Letter

- Cover Letter Text Examples

The key to crafting an eye-catching operations manager cover letter is to feature tangible achievements that convey how you’ve effectively managed teams and enhanced day-to-day operational workflows. Emphasize your ability to create value for prospective employers and build dynamic teams that excel. This guide provides examples and expert insights to help you craft a winning operations manager cover letter.

Operations Manager Cover Letter Templates and Examples

- Entry-Level

- Senior-Level

How To Write an Operations Manager Cover Letter

To write a great operations manager cover letter, you need to illustrate your most impressive career achievements. Feature tangible examples of you improving operational efficiency, reducing costs, and driving positive business outcomes. Demonstrate your ability to manage diverse teams and develop effective standard operating procedures. Below, we’ll walk you through each step of building a stand-out operations manager cover letter:

1. Contact information and salutation

List all essential contact information at the top of your operations manager cover letter, including your name, phone number, email, and LinkedIn URL. Greet the hiring manager by name — Mr. or Ms. [Last Name]. If you can’t find the hiring manager’s name, use a variation of “Dear Hiring Manager.” This shows that you’ve researched the company before applying and conveys your genuine interest in the opportunity.

2. Introduction

Open your operations manager cover letter with an impactful introduction. Emphasize your years of experience in operations and anchor your introduction with a notable accomplishment that demonstrates the value you can bring to the organization. This will draw the hiring manager’s eye and entice them to explore your background more thoroughly.

Notice how this candidate provides a compelling overview of their career in the opening paragraph of their operations manager cover letter. Managing operations in a high-traffic environment such as an airport requires exceptional leadership skills. This additional context also strengthens the impact of the customer satisfaction increase.

I’m reaching out in regard to the operations manager position at Delta Airlines. During my time with Detroit Metropolitan Airport, I oversaw daily frontline operations for a major airport and successfully increased customer satisfaction ratings from 70% to 87% over two years. I can achieve similar success for your organization in the operations manager role.

3. Body paragraphs

In the body of your operations manager cover letter, include up to two paragraphs that describe your most impactful achievements and qualifications. Mention something specific about the organization’s reputation or culture and why this draws you to apply for the position. Include a mix of accomplishments that demonstrate your leadership capabilities and talent for driving operational excellence. Consider including a list of bullet points to break up the text on the page.

In the example below, the candidate quantifies their achievements to give the hiring manager a sense of scope. In addition to reducing overhead costs, the applicant highlights the number of staff they managed. They also draw attention to challenges they overcame during the pandemic, which had a unique impact on the hotel industry. By delving deeper into your professional experience, you can add a dynamic element to your operations manager cover letter.

Marriott’s reputation as a brand that truly values the guest experience draws me to apply for this opportunity. As an operations manager at Four Season Hotel, I overcame numerous challenges during the COVID-19 pandemic to ensure safety and improve guest satisfaction. I can achieve similar results for your company based on my career achievements:

- Managed day-to-day operations and functions for a high-end hotel generating $10 million in gross annual revenue, including staffing, vendor management, and guest relations

- Led a team of over 80 personnel, coordinated workflows, and identified operational enhancements to reduce overhead costs by 35%

- Spearheaded change management and training initiatives to improve service delivery and enhance the guest experience, resulting in a 20% increase in satisfaction scores

4. Operations manager skills and qualifications

Rather than providing a long list of skills on your operations manager cover letter, use this opportunity to show the hiring manager how you’ve applied these skill sets to achieve results throughout your career. Focus on highlighting specific keywords from the job posting whenever possible. Below, you’ll find a variety of skills to consider adding to your operations manager cover letter:

| Key Skills and Qualifications | |

|---|---|

| Agile methodology | Budget management |

| Change management | Communication |

| Continuous improvement | Cost management |

| Cross-functional leadership | Data analysis |

| HR management | Operational excellence |

| People management | Process improvement |

| Profit and loss (P&L) management | Project management |

| Standard operating procedures (SOPs) | Strategic planning |

| Strategy development | Talent acquisition |

| Team management | |

5. Closing section

End your operations cover letter strongly with a call to action (CTA) inviting the hiring manager to interview you. Reinforce how your industry expertise can help improve operations for the organization you’re targeting. In the last sentence, be sure to thank the hiring manager for their time and consideration.

I would like to schedule an interview to tell you more about how my operations management experience can help Delta Airlines continue to excel as a customer-first organization. Feel free to contact me regarding any additional questions you have about my background. I appreciate your time and consideration.

Best regards,

Anthony Gentile

Operations Manager Cover Letter Tips

1. quantify your achievements as an operations manager.

Although operations management roles vary across industries, incorporating hard numbers, monetary figures, and metrics is the best way to help your achievements stand out. In the example below, the candidate has a strong background in managing operations for large warehouses and production facilities. Emphasizing the impact of their contributions to both production output and safety compliance makes them a compelling candidate for roles in this industry:

- Managed all aspects of plant operations for two facilities with over 200 staff, identified tactical solutions to drive operational excellence, and enhanced production by output by 15%

- Established a strong safety culture and implemented new training programs to ensure compliance with OSHA standards, which successfully reduced workplace accidents by 30%

- Introduced new quality assurance procedures and audits to reduce product defects

2. Highlight your leadership capabilities

Overseeing daily operations for any type of business requires strong people management and communication skills. As you write your cover letter, showcase how you’ve built, trained, and led diverse teams to drive operational excellence. This sends a clear message that you can improve productivity for your employers and are an ideal culture fit for their team.

3. Align your cover letter with the job description

To grab the hiring manager’s attention, carefully align your cover letter with the job description. For example, if a company is seeking a candidate with an extensive background in customer success, you’d highlight examples of refining operations and training programs to improve client satisfaction. If an organization is looking for an operations manager who can reduce overhead costs, emphasize how you’ve successfully refined workflows and processes to support business growth.

Operations Manager Text-Only Cover Letter Templates and Examples

Anthony Gentile Operations Manager | [email protected] | (123) 456-7890 | Detroit, MI 12345 | LinkedIn

January 1, 2024

Lori Taylor Hiring Manager Delta Airlines (987) 654-3210 [email protected]

Dear Ms. Taylor:

I’m reaching out about the operations manager position at Delta Airlines. During my time with Detroit Metropolitan Airport, I oversaw daily frontline operations for a major airport and successfully increased customer satisfaction ratings from 70% to 87% over two years. I can achieve similar success for your organization in the operations manager role.

Delta Airlines’ reputation as an industry leader in customer service innovation is what draws me to apply for this opportunity. Throughout my career, I’ve led diverse cross-functional teams to enhance the customer experience and ensure passenger safety. My leadership capabilities would be an asset to your company based on my previous achievements:

- Oversaw daily frontline operations for a major airport, managed a team of over 70 frontline staff, coordinated daily workflows and scheduling, and provided a high-quality customer experience, including identifying resolutions to escalated issues

- Delivered coaching and training to team members to build a collaborative work culture centered on safety and customer service, resulting in an 87% rating on customer surveys

- Conducted operational audits and root cause investigations to ensure the safety of team members and passengers during boarding and flights

I would like to schedule an interview to tell you more about how my operations management experience can help Delta Airlines continue to excel as a customer-first organization. Feel free to contact me regarding any additional questions on my background. I appreciate your time and consideration.

Skyler Thompson Operations Manager | [email protected] | (123) 456-7890 | Seattle, WA 12345 | LinkedIn

Hector Santos Hiring Manager Haden Medical Device Co. (987) 654-3210 [email protected]

Dear Mr. Santos:

I’m interested in applying for the operations manager position with Haden Medical Device Co. that I found on LinkedIn. As you can see from my attached resume, I have eight years of experience overseeing large production facilities for leading medical equipment providers. My leadership capabilities and industry knowledge will allow me to create value for your organization.

Haden Medical Device Co.’s reputation for delivering cutting-edge medical equipment products draws me to apply for this opportunity. During my time with Seattle Med Solutions, I spearheaded efforts to automate assembly processes, which saved the company over $300,000 in labor expenses. I can achieve similar results for your team based on my career achievements:

I look forward to telling you more about how my experience in high-volume production environments could help drive operational excellence at Haden Medical Device Co. Feel free to contact me via phone or email at your convenience. Thank you for your time and consideration.

Skyler Thompson

Meera Patel Operations Manager | [email protected] | (123) 456-7890 | Detroit, MI 12345 | LinkedIn

Tyrone Jackson Hiring Manager Marriott (987) 654-3210 [email protected]

Dear Mr. Jackson:

I’m interested in applying for the general manager job with Marriott that I found on LinkedIn. With over 10 years of experience within the hospitality industry, I have a proven track record of leading change management initiatives to revamp operations for luxury hotels. My extensive background in operations would be a strong asset to your team in this position.

Marriott’s reputation as a brand that truly values the guest experience attracts me to apply for this opportunity. As an operations manager at Four Season Hotel, I overcame numerous challenges during the COVID-19 pandemic to ensure safety and improve guest satisfaction. I can achieve similar results for your company based on my career achievements:

I hope to speak with you further regarding how my operations management experience in hospitality can help Marriott continue to improve the guest experience. Feel free to contact me via phone or email at your convenience. I appreciate your time and consideration.

Meera Patel

Operations Manager Cover Letter FAQs

Why should i include an operations manager cover letter -.

While many operations manager jobs won’t require a cover letter, submitting one certainly won’t hurt your chances of landing the interview. This gives you an opportunity to display your genuine interest in the position and why you want to work for this specific company. This small touch can sometimes differentiate you from other applicants during the hiring process.

How long should my cover letter be? -

It’s generally best to keep your cover letter concise, limited to no more than three or four paragraphs. Overwhelming the reader with information risks drawing their attention away from your strongest qualifications and achievements. Providing a brief yet compelling cover letter is a much more effective way to generate interviews.

How do I make my cover letter stand out? -

Rather than simply reiterating every detail from your resume, include unique details in your cover letter that provide added context for your achievements and career experience. Emphasize your passion for your industry and the types of challenges you overcame to positively impact an organization’s operational efficiency.

Craft a new cover letter in minutes

Get the attention of hiring managers with a cover letter tailored to every job application.

Frank Hackett

Certified Professional Resume Writer (CPRW)

Frank Hackett is a professional resume writer and career consultant with over eight years of experience. As the lead editor at a boutique career consulting firm, Frank developed an innovative approach to resume writing that empowers job seekers to tell their professional stories. His approach involves creating accomplishment-driven documents that balance keyword optimization with personal branding. Frank is a Certified Professional Resume Writer (CPRW) with the Professional Association of Resume Writers and Career Coaches (PAWRCC).

Check Out Related Examples

Customer Success Manager Cover Letter Examples and Templates

Manager Cover Letter Examples and Templates

Supervisor Cover Letter Examples and Templates

Build a resume to enhance your career.

- Should Your Cover Letter and Resume Templates Match? Learn More

- How to Include Personal and Academic Projects on Your Resume Learn More

- Supervisor Resume Examples Learn More

Essential Guides for Your Job Search

- How to Land Your Dream Job Learn More

- How to Organize Your Job Search Learn More

- How to Include References in Your Job Search Learn More

- The Best Questions to Ask in a Job Interview Learn More

- Resume Templates Simple Professional Modern Creative View all

- Resume Examples Nurse Student Internship Teacher Accountant View all

- Resume Builder

- Cover Letter Templates Simple Professional Modern Creative View all

- Cover Letter Examples Nursing Administrative Assistant Internship Graduate Teacher View all

- Cover Letter Builder

- Operations Manager

Operations Manager cover letter example

Primary purpose

Secondary purpose, how to land an entry-level operations manager position.

With a great operations manager cover letter, you can quickly rise above the rest to prove your problem solving skills, commitment to stakeholders and business acumen. That new job can quickly be yours – if you know how to sell yourself in your operations manager cover letter.

Without an operations manager, a business would never get past the ideation phase. An operations manager oversees all the necessary steps to make a product or service a reality in the hands of a consumer.

Operations managers handle a wide range of tasks from delegating duties to designing production systems and calculating materials cost and pricing. A great operations manager is vital to the success of a company so hiring managers will be looking for the best of the best when it comes time to fill this position.

With this operations manager cover letter example plus Resume.io’s tips, tools and cover letter templates , you’re never alone on the journey to land your dream position. We’ll walk you through the steps to craft a great operations manager cover letter from start to finish.

This operations manager cover letter example along with our adaptable sample sentences will:

- Show you how a well-crafted cover letter can significantly boost your chances of landing the position

- Offer free examples, samples and templates to simplify the writing process

- Explore tips and tricks to land an operations manager job even with no experience

- Help you avoid the biggest cover letter mistakes and catch a recruiter’s attention

Before we dive further into writing the perfect cover letter, you’ll want to make sure that your resume is in top shape. Check out our operations manager resume example , plus our comprehensive guide on how to write a resume for tons of tips on creating an outstanding resume.

Operations manager cover letter sample and purpose

While most job seekers understand what a resume is, fewer are as aware of the specific rules of cover letter writing. The cover letter, sometimes called an application letter, can feel like a structureless document that the employer may not even appreciate. However, that couldn’t be further from the truth. In the following subsection, we’ll explain why your cover letter should receive just as much attention as your resume.

But first let’s look at some general guidelines for the perfect cover letter:

- Keep your length to a one-page maximum (about 200 to 400 words)

- Expand on soft skills like personality and leadership style

- Discuss achievements and skills with concrete examples

- Match your tone and writing to the company’s

- Pay attention to your visual presentation and formatting

- Rehash everything on your resume

- Include hobbies or unrelated activities

- Go wild with colors or design elements, especially in formal industries

- Come across as arrogant or entitled

Your cover letter is your chance to make a personal connection with the employer by using the most relevant examples that show how you’d perform in the company’s work environment. While great writing is essential, you’ll also need professional formatting to convey your experience and mastery of the field. You can find tons of tips and advice on fonts, colors and templates in our overall guide on cover letters .

If you’re applying for an operations manager position, then this likely isn’t your first time writing a cover letter. While all your previous positions have prepared you for this moment professionally, the same isn’t necessarily true for your previous applications.

That’s because a lot of candidates see the cover letter as a chore – just one more hurdle to jump before submitting their application. But the boring, generic cover letters that result from this mindset likely don’t do the applicants any favors.

When crafted with care and reflection, a cover letter is a secret weapon. It allows you to maneuver past other candidates, even those with more years of experience, and prove to a hiring manager that it’s worth taking a shot on you.

An operations manager who name drops a lot of big companies but can’t explain how they created a successful operation might find themselves neck and neck with a young candidate who can clearly demonstrate a track-record of achievement. And once you find yourself in the interview round, it’s anyone’s game.

A great cover letter is all about maximizing your chances. With confidence, professionalism and the right tools, that perfect position can be yours.

The importance of tailoring your cover letter

One of the most common traps that even candidates for high-level positions fall into is failing to customize their cover letter for each employer they apply to. Unfortunately, a generic, one-size-fits-all cover letter just won’t cut it – especially not for an operations manager role where the position is molded to fit the company and type of production.

To truly have the best chance of getting a job interview, it is essential that you customize your cover letter with the most relevant achievements, examples, skills and even personality traits for the specific employer and position. It may take a bit of extra effort, but the time invested will pay dividends when the recruiter notices your commitment.

Best format for an operations manager cover letter

Understanding the elements of a good cover letter is one of the best things you can do to make sure your application checks off all the boxes and catches the eye of the hiring manager. The sections below tend to stay relatively the same regardless of the industry in which you plan to work. Here are the key components:

- The cover letter header

- The greeting / salutation

- The cover letter intro

- The middle paragraphs (body of the letter)

- The ending paragraph of your cover letter (conclusion and call-to-action)

You can find even more details on each of these sections, plus free sample sentences, in our overall example: How to Write a Cover Letter .

Cover letter header

Your operations manager cover letter header has two important jobs. The first is to list all the necessary identifying information in case your application floats from desk to desk. Nothing dashes your chances more than having a recruiter frustrated that they don’t know how to contact you.

Include your personal data like your name, phone number and email address. Your LinkedIn may also be important depending on the company, but be careful not to overload the header with too much information.

Your header also plays a key role in the formatting of your letter. This is one of the only sections where you’ll be able to customize the design and even add a touch of color if appropriate. For an upper level position like operations manager, you’ll want to make sure your visual presentation matches the tone of the company. A cover letter template may be able to help.

The goal of this section: Keep your name and contact information at the forefront of your document, create attractive formatting that is professional and eye-catching

Align document styles

For lower-level positions, aligning document styles is an option to make your application a bit more professional. For an operations manager, however, it’s practically a must. Aligning document styles means matching your cover letter and resume header and page layout. This simple step makes your application appear cohesive and polished and helps your documents stand out in the hiring manager’s mind.

If you don’t have the time or energy to tackle page design yourself, a resume template and corresponding cover letter template can make the process quick and easy. Just choose a style that aligns with the company’s branding and tone so as to show that you understand their needs and image. For operations managers, we recommend the Professional category of our free cover letter templates .

Cover letter greeting

The greeting of your operations manager cover letter is a small but powerful section. Your most important objective here is to address the hiring manager or letter recipient by name to establish the personal connection and respectful tone that you will maintain throughout.

For most formal industries, the traditional “Dear” followed by the correct salutation and last name is the most appropriate choice. However for very modern companies with innovative work environments, you might opt for a more casual greeting or even a first name.

The goal of this section: Create a friendly and respectful tone by addressing the hiring manager by name

The importance of names and addressed greetings

As mentioned above, addressing the hiring manager by name is one of the most important elements of a customized and effective cover letter. This simple step helps show your interest in the position and that you put the time in to get to know the company before applying. In fact, science has even proven that humans have a positive reaction to hearing their own names – all the more evidence to incorporate this tip into your cover letter.

However, in large companies with large HR teams, finding the exact name of the person or people who will be responsible for evaluating your application can be downright impossible. If this is the case, there’s no need to worry. You can try using a more general greeting. “Dear Hiring Manager” is alright if you’re sure only one person will be reading. “Dear (Company Name) Hiring Team” or even “Hiring Family” can work better for large companies.

Cover letter introduction

Your operations manager cover letter introduction is the first sentence or two of your cover letter. Hiring managers have very little time to evaluate each application so if your introduction isn’t top-notch there’s a good chance they won’t keep reading. Not to worry.

You can easily knock this section out of the park by using an anecdote, exciting personal statement or relevant statistic to grab attention and lead the reader right into the body of your cover letter.

The goal of this section: Avoid a generic opening and create interest with an anecdote, statistic or skill that flows into the next section

Cover letter body

The body of your operations manager cover letter makes up the bulk of your document. Here, you’ll expand on your achievements, skills and visions as an operations manager. Since this section contains the majority of the information, you can ease the writing process by dividing it in half.

In the first section, use the STAR method to describe a S ituation, the T ask required of you, your A ction and the positive R esult that followed. Since operations manager duties can vary so widely, it’s a good idea to use the job description and research from the company website to narrow down your examples to only the most relevant and impactful for your potential employer.

In the second body paragraph, discuss your strongest skills including just a few hard skills if essential to the position. Discuss your vision or potential contribution to the company without sounding presumptuous or critical.

The goal of this section: Give short examples of your previous achievements and successes, discuss your most noteworthy strengths and the ideas you’d bring to the potential employer

How to close an operations manager cover letter (conclusion and sign-off)

Your operations manager cover letter is almost written! Before you pop open that champagne, you’ll need to wrap it up with your conclusion and signature. Express your interest and enthusiasm for the position and invite a hiring manager to get in touch in the Call to Action.

Then choose the most appropriate signature based on the tone of your greeting and your relationship with the employer. “Warm regards,” “Sincerely” or “Thank you” can all make great options.

The goal of this section: Create a positive and respectful Call to Action that leaves a hiring manager wanting to get in touch, sign off with the most appropriate signature for your potential employer

Entry level operations manager cover letter – tools and strategies

While on the job search for an operations manager job, there are a few key qualities you’ll want to convey:

- Management skills : Motivation, negotiation, conflict resolution and time management – being able to manage processes and the people behind them are at the core of this position. Give examples that show how you lead with authority while still considering your teams’ needs.

- Communication skills : You’ll be dealing with multiple departments within the company – if not all of them. The ability to stay organized and communicate clearly and professionally are musts. Show off your communication skills through error-free writing, strong action verbs and easy-to-understand examples.

- Business administration skills : While in some companies the operations manager is the day-to-day person running things on the ground, other positions require a wide view and the ability to correctly document production, deal with HR policies and manage business operations. Make sure to get an indication of what type of position you’re applying for before writing your cover letter.

- Hard skills : Budgeting, scrum, six sigma, regulatory compliance: your hard skills make it all happen. While they shouldn’t be the focus of your cover letter, examples that show how you incorporate essential knowledge along with soft skills will be a plus on any operations manager cover letter.

Although operations managers work at the highest levels of big companies and international organizations, that doesn’t mean that every operations manager position requires years of systematic career building. In fact, small companies also need operations managers who can handle production and manage workflow. These positions can make great entry-level opportunities, especially for recent grads from MBA or other management programs.

So how can you land an entry-level operations manager position? It all comes down to proving your vision and aligning yourself with the company goals. As always, understanding the employer’s needs and the potential responsibilities is the first step to crafting a great cover letter, especially for an entry-level position. Then consider the experience you do have. What projects or achievements make you believe you’d be a great operations manager? What skills did you use for those tasks that are applicable to the new position?

You can also play your youth to your advantage. Are you a quick learner who implements new technology without hesitation? Do you take feedback well and seek out expert advice? Are you committed to innovation and taking calculated risks? These traits are essential for the modern operations manager, yet they may be missing from applicants who are set in their ways after years of experience.

Time to get specific

When you’re applying for any operations manager role, but especially an entry-level one, you’ll want to give key statistics and numbers that prove you’re able to drive results. Of course, impressive achievements should be at the top of the list, but even if you don’t have much experience you can still give details that help make your application stand out in a hiring manager’s mind.

Some sample sources of numbers for your cover letter:

- The size of the team you managed

- The number or products produced

- The value of products produced

- Measures of production efficiency

- Measures of business success that can be partly attributed to operations

- Brand awareness raised

- Budget reduced or efficiency increased

- Shareholder benefits

Common mistakes in an Operations Manager cover letter

- Not understanding the company needs : The operations manager role covers a wide variety of skills and can look completely different depending on the company. Your cover letter could not only miss the mark but actually decrease your chances of landing the position if it’s not written with the employer’s specific needs in mind.

- Too much focus on hard skills : Don’t get us wrong – hard skills are a necessary component of the job. But they’re not everything. Make sure your cover letter sounds like a human wrote it, with confidence and leadership abilities that will set you apart from other candidates with the same technical skills.

- Grammar and spelling mistakes : Nothing makes you look unprofessional faster than poor grammar and typos. How can a company trust you’ll communicate professionally if you can’t even do it on your cover letter? Luckily these little errors don’t have to ruin everything. Make sure to use spell check or ask a friend to proofread your application.

- Poor formatting : Believe it or not, visual presentation often counts just as much as good writing. Your header and pay layout are the first impression a hiring manager will have of you so make sure they are professional and aligned with the company’s image and branding.

Key takeaways

- Your cover letter should expand on the key experiences and achievements of your resume, not just rehash everything you’ve ever done.

- A thoughtful, customized cover letter is one of the best things you can do to increase your chances of landing the position. Make sure to include one as part of a great application.

- Follow the trusted cover letter structure and make sure to address the letter recipient by name in your cover letter greeting if at all possible.

- A great cover letter starts with understanding the company’s needs. Give concrete examples of your achievements with numbers and statistics that will make a hiring manager take notice.

- Don’t overlook professional formatting. A matching resume template and cover letter template can help you create a great layout in just a few clicks.

For more cover letter ideas, check out these related administrative cover letter samples:

- Administrative cover letter example

- Administrative officer cover letter sample

- Office administrator cover letter example

- Office manager cover letter sample

- Sales manager cover letter example

Build your cover letter effortlessly with resume.io’s tools: an advanced online cover letter maker , writing auto-suggestions, professional recruiter-approved designs and more!

Free professionally designed templates

Resume Templates

Resume samples

Create and edit your resume online

Generate compelling resumes with our AI resume builder and secure employment quickly.

Write a cover letter

Cover Letter Examples

Cover Letter Samples

Create and edit your cover letter

Use our user-friendly tool to create the perfect cover letter.

Featured articles

- How to Write a Motivation Letter With Examples

- How to Write a Resume in 2024 That Gets Results

- Teamwork Skills on Your Resume: List and Examples

- What Are the Best Colors for Your Resume?

Latests articles

- Key Advice Before You Sign Your Next Work Contract in 2024

- Resume Review With AI: Boost Your Application with Ease

- Top AI Skills for a Resume: Benefits and How To Include Them

- Top 5 Tricks to Transform Your LinkedIn Profile With ChatGPT

Dive Into Expert Guides to Enhance your Resume

Operations Manager Cover Letter Example

Securing a position as an Operations Manager requires a meticulously crafted cover letter that leaves no stone unturned. Learn how to effectively enhance your application with our sample cover letters, along with our expert advice and proven strategies for optimization.

Operations Manager Example Cover Letter

Looking to secure your dream job as Operations Manager? A well-crafted cover letter is essential in setting yourself apart from the competition. With a strong cover letter, you can highlight key skills, such as accuracy, efficient time management, organization, and problem-solving .

By effectively communicating your qualifications and matching them with the employer’s requirements, you can create a compelling cover letter that paves the way for a successful job application.

Keep reading to find out more about:

- How to show your passion for operations management

- 3 skills experienced Operations Managers must list on their cover letter

- The one skill entry-level candidates must have to get their first opportunity

- How to increase your chances of getting an interview by writing a powerful closing statement

Embrace the power of cover letter writing and unlock exciting opportunities in operations management, propelling your career to new heights.

Let’s begin!

[ Hiring Manager’s name ]

[Company name]

[Company address]

Dear Mr/Ms. [Hiring Manager Name]

As an Operation Manager with over 6 years of experience and a strong history of managing the functions of small and medium-sized retail businesses, I couldn’t resist the opportunity to apply for the position being offered by [Company]. On reading the job description, I knew that I was just the candidate that you are looking for.

Having studied a Bachelor’s Degree in Business Management and built on that foundation with practical expertise in planning budgets, fostering teamwork, and setting company goals; I am able to take a 360º view when managing projects, with a careful eye on risk vs reward strategies. This has led to major successes in my career so far.

In my present position with [Current Company], I led over 5 major projects to success, running them from absolute start-up to full implementation. Each was kept well within budget and achieved an average ROI of over 10% within 1 year of launch.

I am eager to build on this knowledge and take my success even further with [Company].

Please find my resume enclosed, which provides more information on the work I’ve done up to this point in my career. I would, of course, be more than happy to elaborate on the details further in a face-to-face meeting.

Thank you once again for considering my application. I look forward to hearing from you in the future.

[Name] [Address] [Phone number] [Email address]

3 Ways to Show Your Passion for Operations Management

Operations manager roles rank 11th on US News’ Best Business Jobs list. With higher than average salaries, it’s no wonder that competition can be quite fierce. One way to stand out from other candidates is by conveying passion for the role.

Employers seek candidates who are not only skilled but also enthusiastic and dedicated to driving success.

Follow these practical and empowering tips to display your passion and make your cover letter a success:

Connect with the company’s values

Research the company and align your own values with theirs. Highlight how your passion for operations management aligns with the company culture and objectives.

This shows recruiters you are genuinely invested in contributing to the organization’s success.

“I was immediately drawn to XYZ Company’s focus on sustainability and ethical business practices. As an operations manager, I’m passionate about ensuring that production processes are not only efficient but also environmentally responsible.”

Feature your proactive mindset

Operations managers need to be proactive problem solvers. Mention instances where you identified issues or challenges, and proactively implemented solutions.

This demonstrates your commitment to finding innovative ways to drive efficiency and achieve goals.

“During my tenure as operations manager at ABC Company, I observed that our inventory management system was causing delays in production. I immediately identified the issue and developed a new logistics management plan that reduced lead times within three months. My proactive approach helped streamline our internal operations and increased customer satisfaction by 20%.”

Discuss ongoing development

Show that your passion for operations management goes beyond your current level of expertise. Highlight any continuous learning or professional development efforts, such as attending relevant workshops, earning certifications, or staying up-to-date with industry trends.

This conveys your hunger for growth and your willingness to stay ahead in the field.

“I’m continuously improving my operations management skills. Last year, I attended a Lean Six Sigma training program, and I’m currently pursuing a PMP certification to further develop my project management proficiency. My dedication to professional development will allow me to implement the latest industry trends and drive continuous improvement in your organization.”

By incorporating these strategies into your Operations Manager cover letter, you can authentically convey your enthusiasm for the role. A passionate candidate stands out, and with our practical advice, you can confidently present yourself as the perfect fit for the position.

2 Must-Have Skills to Add to Your Operations Manager Cover Letter

Crafting an exceptional cover letter for Operations Manager requires more than just a generic template. Employers seek candidates who possess specific skills that will drive success in this role.

Get ready to supercharge your cover letter and stand out in the job market.

1. Leadership

As an operations manager, strong leadership skills are essential for effectively managing teams and driving results. Highlighting your ability to lead and inspire others can demonstrate your potential to excel in this role.

Here’s an example of how you can do this in your cover letter:

“In my previous role as operations manager at XYZ Company, I successfully led a team of 20 employees to consistently meet and exceed production targets. By implementing a collaborative and empowering leadership style, I fostered a positive and high-performing team culture that resulted in a 15% increase in productivity within six months.”

2. Strategic Planning

Operations managers are responsible for developing and implementing strategic plans to optimize operations and achieve business objectives. Including your strategic planning abilities in your cover letter can show employers that you have the vision and foresight to drive successful outcomes.

Look at the following example to see how it’s done:

“Throughout my career, I have demonstrated expertise in developing and executing comprehensive operational strategies that drive efficiency and cost savings. At ABC Company, I spearheaded the implementation of a lean manufacturing initiative, resulting in a 25% reduction in production cycle times and a 30% decrease in operational costs within one year.”

With a well-crafted cover letter that includes these must-have skills, you can make a strong impression and increase your chances of landing the Operations Manager role you desire.

How Entry-Level Operation Managers Can Stand Out in a Pool of Applicants

As an aspiring Operations Manager, it is very likely you have some experience under your belt.

The next 2 sections of this article are particularly important to those who want to transition to a high-responsibility role in their operations field but haven’t had the chance yet to prove themselves in a management position.

Entry-Level Operations Manager Sample Cover Letter

Let’s start by reviewing an Operations Manager cover letter example:

I am excited to apply for the Entry-Level Operations Manager position at [Company Name] that was recently posted on your website. As a passionate and driven individual with a Bachelor’s degree in Operations Management, I am confident that I have the skills and experience necessary to excel in this role.

My academic background has provided me with a solid foundation in operations management principles, including process optimization, quality management, and production planning. Additionally, I have completed several projects and internships that have allowed me to hone my skills in data analysis, project management, and team leadership. I am eager to leverage these experiences to drive success at [Company Name].

As an entry-level candidate, I am eager to learn and grow within the organization. I have a track record of quickly adapting to new processes and technologies, and I am committed to ongoing professional development. I am confident that my combination of educational background, experience, and willingness to learn make me a valuable asset to your team.

I am eager to contribute to the growth and success of [Company Name], and I believe that I would be a great fit for the position. Thank you for considering my application. I am excited to show you how I can contribute to your team and hope to be invited to further discuss my qualifications at an interview.

Sincerely, [Your Name]

[Address] [Phone number] [Email address]

Do you also need help with your resume?

Try out our resume builder for Data Entry applicants to give both your resume and letter a boost. You’ll get step-by-step guidance and will be done in just a few minutes.

4 Skills Entry-Level Operations Managers Need to Emphasize on Their Cover Letter

As an entry-level candidate, it’s essential to emphasize a few critical skills that demonstrate your readiness to learn, adapt, and contribute to a new professional environment.

Let’s take a look:

Organization and time management

Recruiters highly value candidates with strong organizational and time management skills. This includes prioritizing tasks, meeting deadlines, and effectively managing multiple projects simultaneously.

Demonstrating these skills in the application process can help convey your ability to handle the fast-paced and dynamic nature of operations management roles.

“In my previous experience at a manufacturing company, I was responsible for coordinating production schedules for three different product lines. To ensure efficiency, I developed a detailed production calendar, prioritizing orders based on customer deadlines and production capacity. By closely monitoring inventory levels and adjusting schedules accordingly, I successfully reduced lead times by 15% and increased on-time delivery rates by 20%.”

Analytical thinking and problem-solving

Operations management requires individuals who can analyze complex situations, identify issues or bottlenecks, and propose effective solutions.

“While working as a part-time operations assistant at a logistics company, I noticed a recurring issue with freight costs exceeding budgeted amounts. To identify the root cause, I conducted a thorough analysis of shipping data and discovered that inefficient route planning was resulting in excessive fuel consumption. I proposed implementing a software solution that optimized route planning, resulting in a 10% reduction in fuel costs within the first month.”

Communication and collaboration

Effective communication and collaboration are essential in operations management, as it involves coordinating and working with cross-functional teams, stakeholders, and external partners.

“As a member of a cross-functional team during a university project, I was tasked with implementing a new quality control process in a manufacturing facility. To ensure the smooth execution of the project, I actively communicated with team members, engineers, and production staff, discussing their needs, addressing concerns, and gathering feedback. By fostering open lines of communication and promoting collaboration, we successfully implemented the quality control process, resulting in a 30% reduction in defects and improved overall product quality.

Project Management

Project management is all about successfully leading and executing complex initiatives. Whether you’ve led a team, managed a project, or played a key role in its success, be sure to include it in your cover letter.

If you have any project management certifications such as PMP , or Agile , make sure to mention them too.

“At XYZ University, I led a sustainability project, demonstrating my project management skills. From planning to execution, I coordinated all aspects, achieving a 20% reduction in campus waste ahead of schedule. This experience equips me to apply these skills effectively as an Operations Manager at your organization.”

Don’t forget to use action verbs and quantifiable achievements to demonstrate the value you’ve brought to previous roles.

Wrap it Up with a Compelling Closing

A cover letter must end on a strong note that leaves a lasting impression. Clearly communicate your desire to move forward in the hiring process by requesting an interview.

Politely and confidently ask for the opportunity to discuss your qualifications further.

“In conclusion, I am enthusiastic about leveraging my proficiency in project management and process improvement to streamline your operations and drive productivity. I am confident that my ability to strategize, problem-solve, and oversee day-to-day operations aligns perfectly with your organization’s objectives. Thank you for considering my application. I look forward to potentially discussing how we can jointly enhance the efficiency and effectiveness of your operations.”

“To conclude, I am excited about the prospect of applying my capabilities in project management, process improvement, and team leadership to fortify the operations at your esteemed organization. Having honed my skills in dynamic, fast-paced environments, I am prepared to navigate and optimize the multifaceted operations integral to your business. I would greatly appreciate the opportunity to discuss this further in an interview. Thank you for your time and consideration.”

Key Takeaways

Follow these takeaways to present yourself as the ideal candidate for the Operations Manager role.

- Feature your ability to lead and manage teams effectively by discussing your management style and successful results.

- Communicate your expertise with project management, problem-solving, and analytical thinking . This demonstrates that you can meet and exceed the demands of the role.

- End your operations manager cover letter with a confident and proactive closing statement that expresses your enthusiasm for the opportunity to contribute to the company’s success. Emphasize your eagerness to discuss how your skills and passion align with their objectives in an interview.

If this seems like a lot to keep track of, or if you still have unanswered questions, our Cover Letter Writing Guide is here to help you navigate through the process.

Trouble getting your Cover Letter started?

Beat the blank page with expert help.

21 Professional Operations Manager Cover Letter Examples for 2024

In your operations manager cover letter, make it clear you understand the role's complexity. Articulate your ability to streamline processes and increase efficiency. Demonstrate your leadership skills and your knack for optimizing team dynamics. Provide examples of how your strategies have positively impacted previous organizations.

All cover letter examples in this guide

Entry-Level Operations Manager

Senior Operations Manager

Experienced Operations Manager

Senior Clinical Operations Manager

Ad Operations Manager

Assistant Operations Manager

Branch Operations Manager

Business Operations Manager

Director Of Operations

Fedex Operations Manager

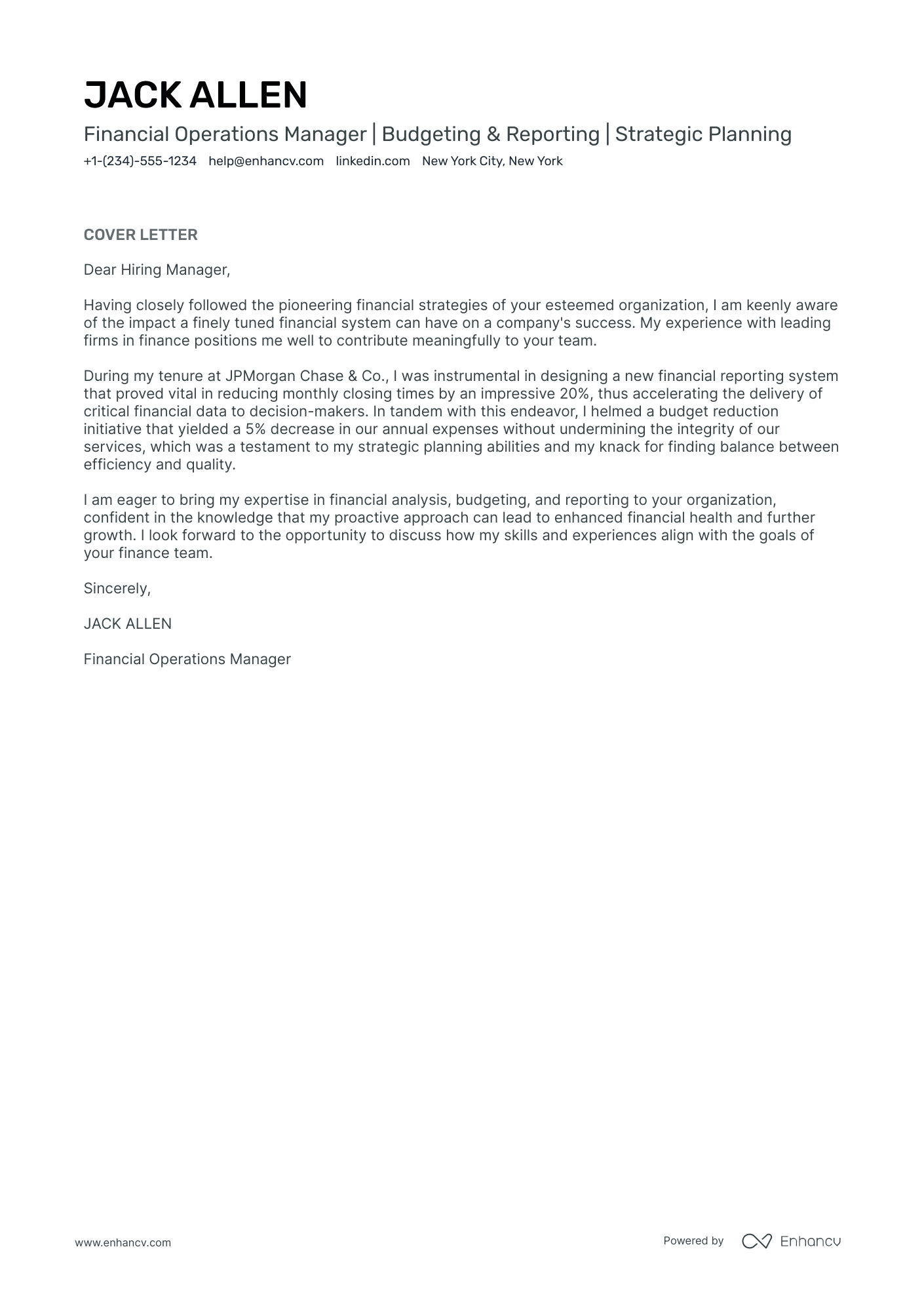

Financial Operations Manager

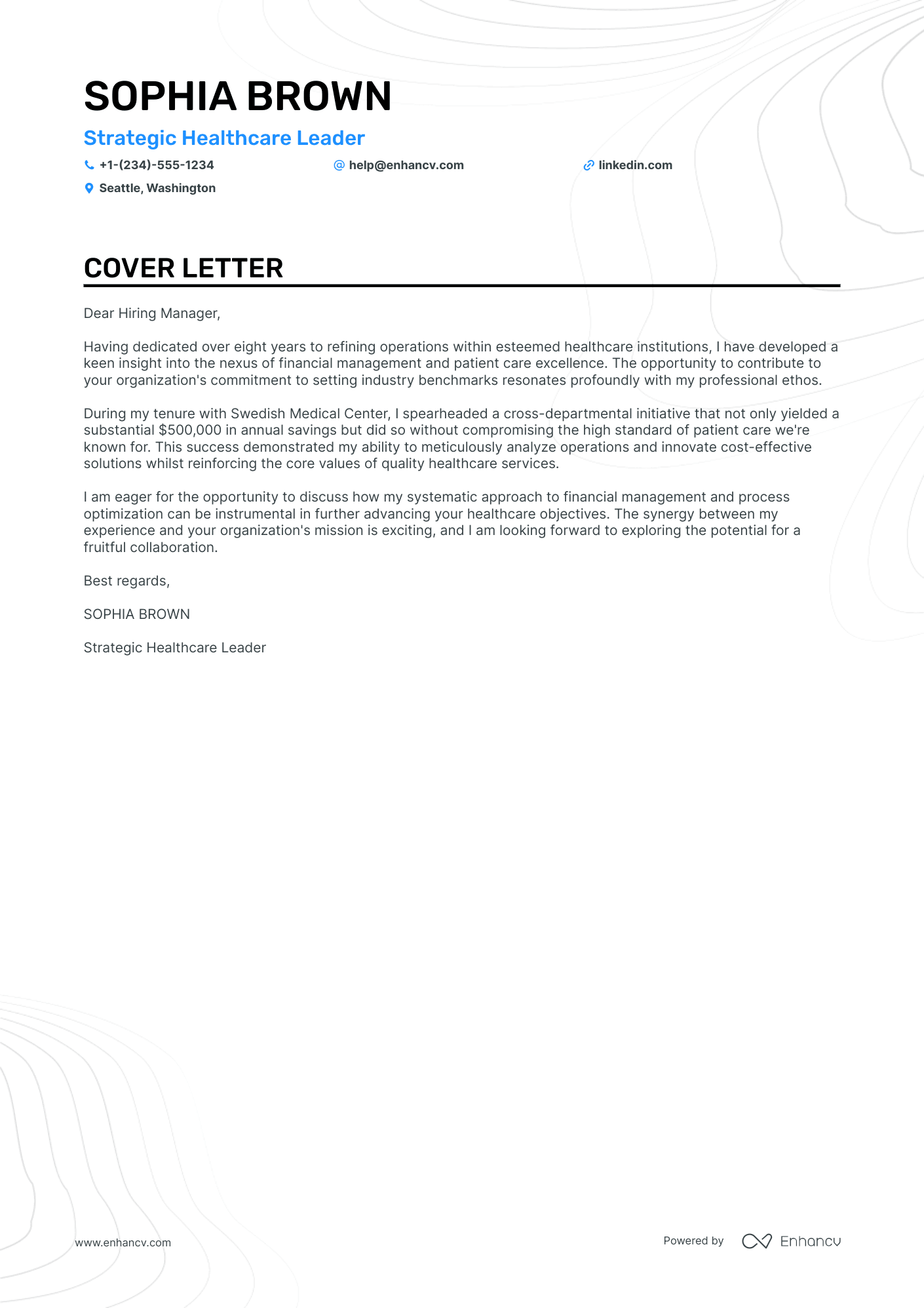

Healthcare Operations Manager

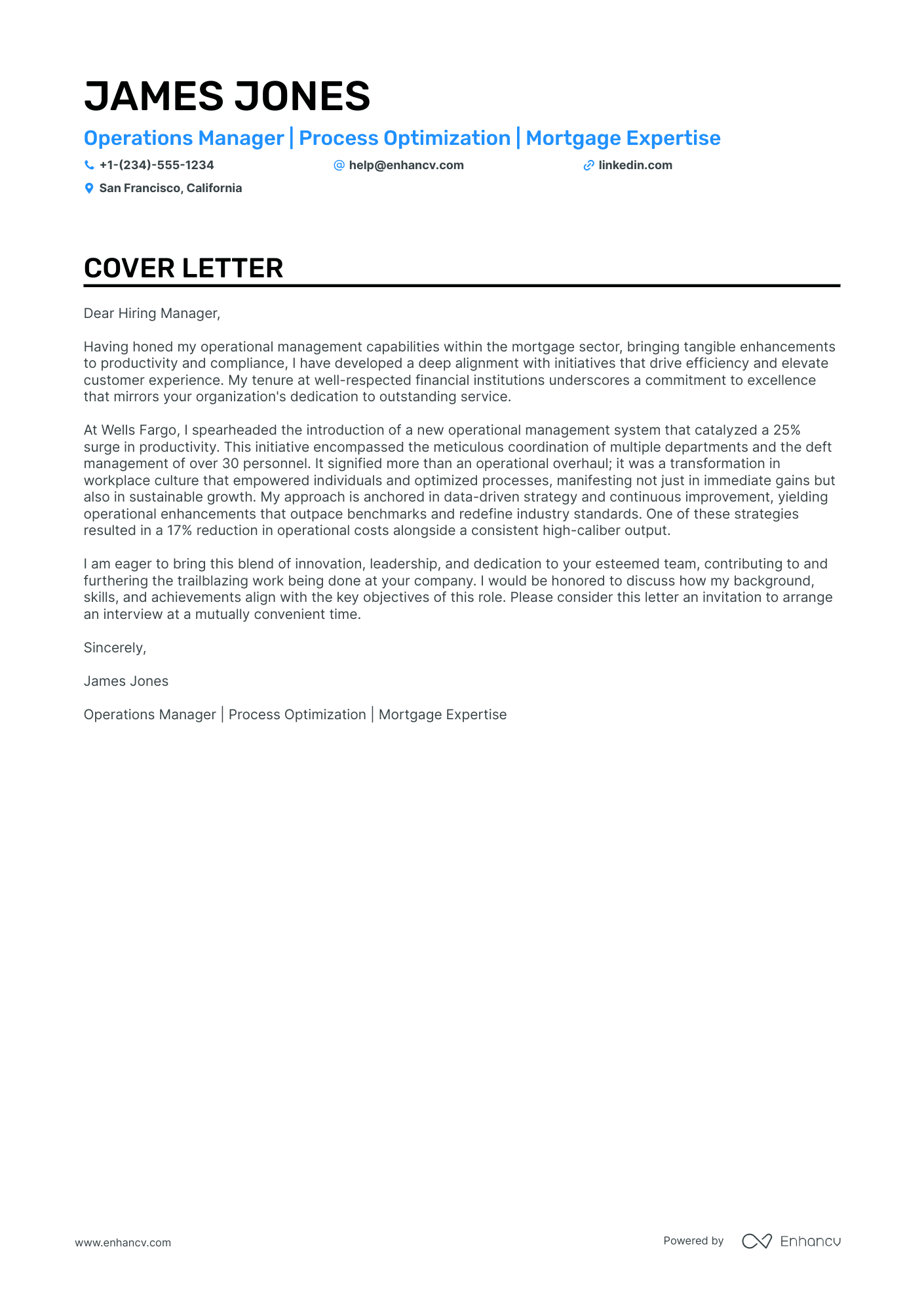

Mortgage Operations Manager

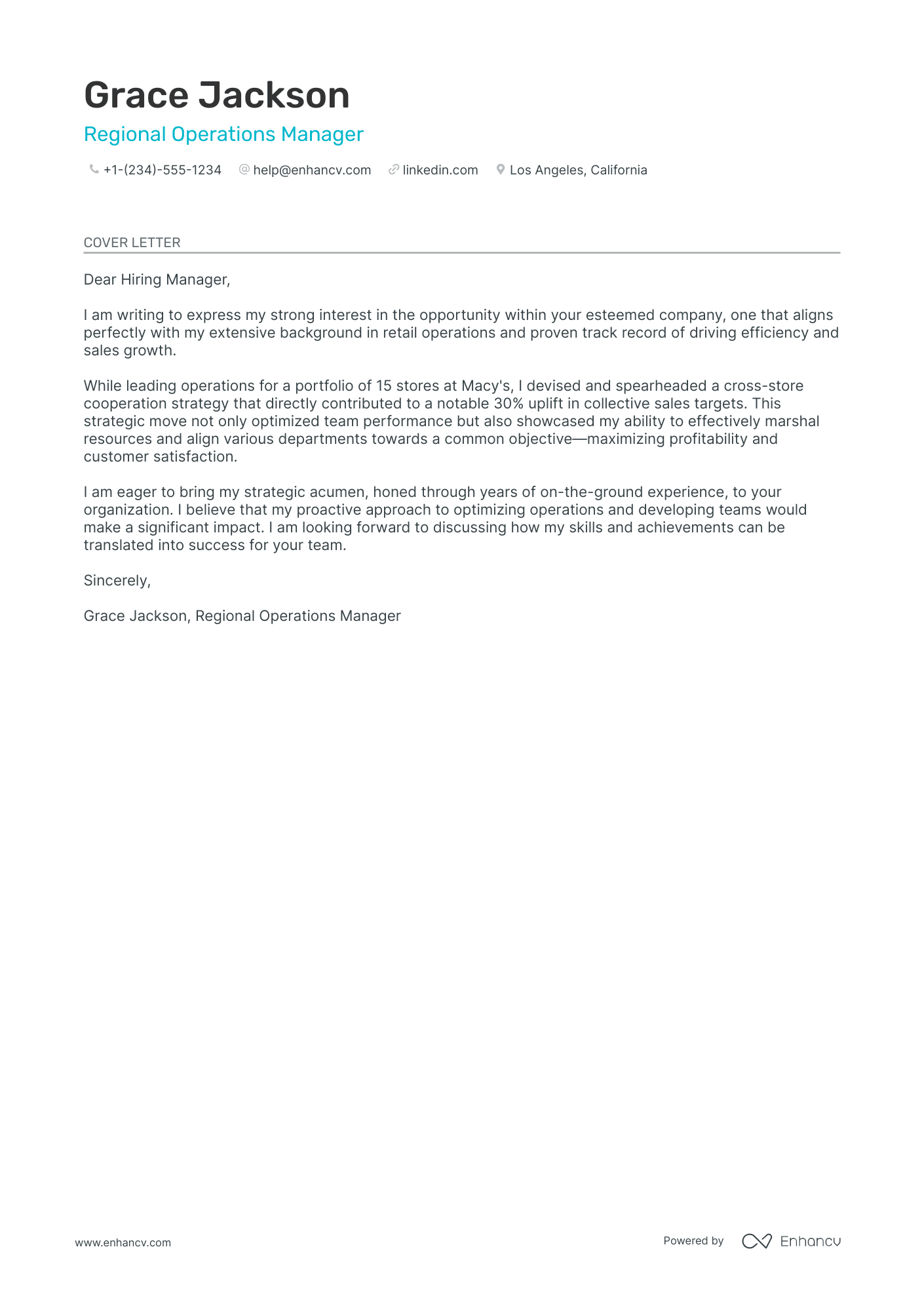

Regional Operations Manager

Restaurant Operations Manager

Transportation Operations Manager

People Operations Manager

Operations Manager Trainee

Distribution Operations Manager

E-Commerce Operations Manager

Cover letter guide.

Operations Manager Cover Letter Sample

Cover Letter Format

Cover Letter Salutation

Cover Letter Introduction

Cover Letter Body

Cover Letter Closing

No Experience Operations Manager Cover Letter

Key Takeaways

By Experience

Writing a compelling operations manager cover letter can be a daunting task, especially when you realize it's a crucial component of your job application. Unlike a resume, your cover letter is the stage to spotlight a professional triumph that showcases your skills. It's a balancing act between formal tone and genuine personality, avoiding worn-out phrases. Remember to keep it concise; a powerful tale of success is best delivered within the confines of a single page.

- Personalize the greeting to address the recruiter and your introduction that fits the role;

- Follow good examples for individual roles and industries from job-winning cover letters;

- Decide on your most noteworthy achievement to stand out;

- Format, download, and submit your operations manager cover letter, following the best HR practices.

Use the power of Enhancv's AI: drag and drop your operations manager resume, which will swiftly be converted into your job-winning cover letter.

If the operations manager isn't exactly the one you're looking for we have a plethora of cover letter examples for jobs like this one:

- Operations Manager resume guide and example

- Senior Operations Manager cover letter example

- Deputy Director cover letter example

- Director of Finance cover letter example

- Senior Director cover letter example

- Operations Supervisor cover letter example

- CCO cover letter example

- Program Director cover letter example

- Director cover letter example

- Entry-Level Operations Manager cover letter example

- Assistant General Manager cover letter example

Operations Manager cover letter example

ANDREW CLARK

+1-(234)-555-1234

- Quantifying Achievements: The cover letter effectively quantifies past achievements (33% improvement in productivity, $50,000 saved), which provides tangible evidence of the candidate's abilities and successes in operations management.

- Relevant Experience: It highlights the candidate's direct experience with operational strategies and workflow optimization, demonstrating their capability to handle similar responsibilities in the prospective role.

- Results-Focused: The language used emphasizes a focus on results, such as setting productivity records and improving the bottom line, appealing to employers who are looking for impact-driven candidates.

- Call to Action: The cover letter concludes with an invitation for an interview, prompting the hiring manager to take action, which is an effective strategy to prompt a response.

Designing your operations manager cover letter: what is the best format

Let's start with the basics, your operations manager cover letter should include your:

- Introduction

- Body paragraph

- Closing statement

- Signature (that's not a must)

Next, we'll move to the spacing of your operations manager cover letter, and yes, it should be single-spaced ( automatically formatted for you in our cover letter templates ).

Don't go for a old-school font (e.g. Arial or Times New Roman), but instead, pick an ATS-favorite like Chivo, Volkhov, or Raleway, to stand out.

Our cover letter builder is also set up for you with the standard one-inch margin, all around the text.

Finally, ensure your operations manager resume and cover letter are in the same font and are submitted in PDF (to keep the formatting in place).

P.S. The Applicant Tracker System (or ATS) won't be assessing your [job] cover letter, it's solely for the recruiters' eyes.

The top sections on a operations manager cover letter

- Header: Include your name, contact information, and date to ensure the recruiter can easily reach you and knows when the application was submitted, which is especially important for operations manager positions where organization and contactability are key.

- Greeting: Address the cover letter to a specific individual, such as the hiring manager, to show attention to detail and personalization, crucial traits for an operations manager who must navigate interpersonal relationships professionally.

- Introduction: Briefly mention your current role, years of experience, and a standout achievement to quickly establish credibility and catch the recruiter's attention, signaling that you are a seasoned operations manager with a history of success.

- Body: Detail your relevant experience with specific examples, such as process improvements or leadership initiatives, to demonstrate your ability to effectively manage operations and lead teams towards organizational goals.

- Closing: Reiterate your interest in the role and the value you can bring to the company, suggesting a follow-up conversation, thereby showing your proactive approach and ability to take initiative—critical qualities for an operations manager.

Key qualities recruiters search for in a candidate’s cover letter

- Proven experience in optimizing operational processes: To demonstrate the ability to streamline workflows for efficiency and effectiveness.

- Strong leadership and team management skills: Essential for motivating employees, delegating tasks, and leading a team to achieve company goals.

- Excellent problem-solving abilities: Critical for identifying operational issues and developing innovative solutions to complex challenges.

- Proficiency in data analysis and performance metrics: To make informed decisions that improve operational performance and business profitability.

- Exceptional communication and interpersonal skills: These are necessary to liaise with various departments, manage stakeholder relationships, and ensure a cohesive organizational effort.

- Experience with budget management and cost control: Demonstrates the capability to manage resources effectively and maintain fiscal discipline within the company.

How to address hiring managers in your operations manager cover letter greeting

Goodbye, "Dear Sir/Madam" or "To whom it may concern!"

The salutation of your operations manager cover letter is how you kick off your professional communication with the hiring managers.

And you want it to start off a bit more personalized and tailored, to catch the recruiters' attention.

Take the time to find out who's recruiting for the role (via LinkedIn or the company page).

If you have previously chatted or emailed the hiring managers, address them on a first or last name basis.

The alternative is a "Dear HR team" or "Dear Hiring Manger", but remember that a "Dear Ms. Simmons" or "Dear Simon," could get you farther ahead than an impersonal greeting.

List of salutations you can use

- Dear Hiring Manager,

- Dear [Company Name] Team,

- Dear [Mr./Ms./Dr.] [Last Name],

- Dear [Position Title] Search Committee,

- Dear [Department Name] Recruiter,

The operations manager cover letter intro: aligning your interest with the company culture

You only have one chance at making a memorable first impression on recruiters with your operations manager cover letter.

Structure your introduction to be precise and to include no more than two sentences.

Here are some ideas on how to write a job-winning operations manager cover letter introduction:

- get creative - show off your personality from the get-go (if this aligns with the company culture);

- focus on your motivation - be specific when you say what gets you excited about this opportunity.

What to write in the body of your operations manager cover letter

Now that you've got your intro covered, here comes the heart and soul of your operations manager cover letter.

It's time to write the middle or body paragraphs . This is the space where you talk about your relevant talent in terms of hard skills (or technologies) and soft (or people and communication) skills.

Keep in mind that the cover letter has a different purpose from your operations manager resume.

Yes, you still have to be able to show recruiters what makes your experience unique (and applicable) to the role.

But, instead of just listing skills, aim to tell a story of your one, greatest accomplishment.

Select your achievement that:

- covers job-crucial skills;

- can be measured with tangible metrics;

- shows you in the best light.

Use the next three to six paragraphs to detail what this success has taught you, and also to sell your profile.

Closing paragraph basics: choose between a promise and a call to action

You've done all the hard work - congratulations! You've almost reached the end of your operations manager cover letter .

But how do you ensure recruiters, who have read your application this far, remember you?

Most operations manager professionals end their cover letter with a promise - hinting at their potential and what they plan on achieving if they're hired.

Another option would be to include a call for follow-up, where you remind recruiters that you're very interested in the opportunity (and look forward to hearing from them, soon).

Choose to close your operations manager cover letter in the way that best fits your personality.

What to write on your operations manager cover letter, when you have zero experience

The best advice for candidates, writing their operations manager cover letters with no experience , is this - be honest.

If you have no past professional roles in your portfolio, focus recruiters' attention on your strengths - like your unique, transferrable skill set (gained as a result of your whole life), backed up by one key achievement.

Or, maybe you dream big and have huge motivation to join the company. Use your operations manager cover letter to describe your career ambition - that one that keeps you up at night, dreaming about your future.

Finally, always ensure you've answered why employers should hire precisely you and how your skills would benefit their organization.

Key takeaways

Writing your operations manager cover letter doesn't need to turn into an endless quest, but instead:

- Create an individual operations manager cover letter for each role you apply to, based on job criteria (use our builder to transform your resume into a cover letter, which you could edit to match the job);

- Stick with the same font you've used in your resume (e.g. Raleway) and ensure your operations manager cover letter is single-spaced and has a one-inch margin all around;

- Introduce your enthusiasm for the role or the company at the beginning of your operations manager cover letter to make a good first impression;

- Align what matters most to the company by selecting just one achievement from your experience, that has taught you valuable skills and knowledge for the job;

- End your operations manager cover letter like any good story - with a promise for greatness or follow-up for an interview.

Operations Manager cover letter examples

Explore additional operations manager cover letter samples and guides and see what works for your level of experience or role.

Cover letter examples by industry

AI cover letter writer, powered by ChatGPT

Enhancv harnesses the capabilities of ChatGPT to provide a streamlined interface designed specifically focused on composing a compelling cover letter without the hassle of thinking about formatting and wording.

- Content tailored to the job posting you're applying for

- ChatGPT model specifically trained by Enhancv

- Lightning-fast responses

A Guide to Finding a Headhunter

How (and when) to add your 2024 promotions to your linkedin profile, how to film a video resume, how to write a military to civilian resume, 40 of the best work at home jobs, should you include your age on your resume.

- Create Resume

- Terms of Service

- Privacy Policy

- Cookie Preferences

- Resume Examples

- Resume Templates

- AI Resume Builder

- Resume Summary Generator

- Resume Formats

- Resume Checker

- Resume Skills

- How to Write a Resume

- Modern Resume Templates

- Simple Resume Templates

- Cover Letter Builder

- Cover Letter Examples

- Cover Letter Templates

- Cover Letter Formats

- How to Write a Cover Letter

- Resume Guides

- Cover Letter Guides

- Job Interview Guides

- Job Interview Questions

- Career Resources

- Meet our customers

- Career resources

- English (UK)

- French (FR)

- German (DE)

- Spanish (ES)

- Swedish (SE)

© 2024 . All rights reserved.

Made with love by people who care.

Operations Manager Cover Letter Example

Cover letter examples, cover letter guidelines, how to format an operations manager cover letter, cover letter header, cover letter header examples for operations manager, how to make your cover letter header stand out:, cover letter greeting, cover letter greeting examples for operations manager, best cover letter greetings:, cover letter introduction, cover letter intro examples for operations manager, how to make your cover letter intro stand out:, cover letter body, cover letter body examples for operations manager, how to make your cover letter body stand out:, cover letter closing, cover letter closing paragraph examples for operations manager, how to close your cover letter in a memorable way:, pair your cover letter with a foundational resume, key cover letter faqs for operations manager.

Start your Operations Manager cover letter by addressing the hiring manager directly, if possible. Then, introduce yourself and briefly mention the position you're applying for. You can also include where you found the job posting. In the first paragraph, it's important to grab the reader's attention. You can do this by stating a key achievement or experience that makes you a strong candidate for the role. For example, "As an Operations Manager with over 10 years of experience in streamlining processes and boosting efficiency in the manufacturing sector, I was excited to see your job posting on XYZ." This not only shows you're a good fit, but also demonstrates your enthusiasm for the role.

The best way for Operations Managers to end a cover letter is by expressing enthusiasm for the opportunity, summarizing their qualifications, and inviting further discussion. They should reiterate their interest in the role and how their skills and experience align with the company's needs. For example, "I am excited about the opportunity to bring my proven track record in improving operational efficiency to your team. I look forward to the possibility of discussing my qualifications further." This ending is assertive and shows eagerness, which can set them apart from other candidates. It's also important to thank the reader for their time and consideration, showing respect and professionalism.

In a cover letter, Operations Managers should include the following: 1. Contact Information: At the top of the cover letter, include your name, address, phone number, and email address. 2. Salutation: Address the hiring manager by name if possible. If not, use a professional greeting such as "Dear Hiring Manager." 3. Introduction: Start by introducing yourself and stating the position you're applying for. Mention how you heard about the job opening. 4. Relevant Experience: Highlight your relevant work experience, focusing on your responsibilities and achievements as an Operations Manager. Use specific examples to demonstrate your skills and how you've used them to drive success in previous roles. 5. Skills: List the skills that make you a strong candidate for the position. These might include project management, process improvement, supply chain management, budgeting, or team leadership. 6. Knowledge of the Company: Show that you've done your research by mentioning something specific about the company that attracted you to the job. This could be their mission, culture, products, or recent achievements. 7. Value Proposition: Explain what you can bring to the company. This could be your ability to improve efficiency, reduce costs, or manage large teams. 8. Closing: In the closing paragraph, express your interest in the position again and your desire to discuss your qualifications further in an interview. Thank the hiring manager for considering your application. 9. Signature: End with a professional closing like "Sincerely" or "Best regards," followed by your name and signature. Remember, your cover letter should complement your resume, not duplicate it. It's your chance to tell a story about your career and show why you're the best candidate for the job. Be sure to tailor your cover letter to each job you apply for, focusing on the skills and experiences that are most relevant to the job description.

Related Cover Letters for Operations Manager

Related resumes for operations manager, try our ai cover letter generator.

Resume Worded | Career Strategy

14 operations manager cover letters.

Approved by real hiring managers, these Operations Manager cover letters have been proven to get people hired in 2024. A hiring manager explains why.

Table of contents

- Operations Manager

- Senior Operations Manager

- Fulfillment Operations Specialist

- Operations Coordinator

- Supply Chain Operations Specialist

- Alternative introductions for your cover letter

- Operations Manager resume examples

Operations Manager Cover Letter Example

Why this cover letter works in 2024, quantifiable achievements.

In this cover letter, the candidate showcases their quantifiable achievements, which is an effective way to demonstrate their impact on previous roles. Use specific numbers to highlight your accomplishments.

Connecting Skills to the Company

By mentioning specific areas where the candidate can apply their experience at Amazon, the cover letter feels tailored and genuine. Show how your skills will directly benefit the company you're applying to.

Demonstrating Relevant Experience

Highlighting relevant experience, such as supply chain management, demonstrates the candidate's suitability for the role and shows they have done their research on the company's needs.

Enthusiasm for the Company

Expressing excitement about working with the company's technology and contributing to its innovation conveys genuine interest in the role and passion for the industry. Be specific about what excites you about the company.

Showcase Your Impact

When you mention that you've reduced operational costs by 15% within a year, it not only highlights your achievements but also gives a measure of the impact you've had. This is real, quantifiable evidence of your capacity to deliver results, and it's exactly what recruiters are looking for.

Relate Achievements to the Role

Improving delivery times by 20% at your previous job is a significant achievement. But the real magic here is how you've related this achievement to the prospective job at Amazon. This shows you understand what the job entails and have a proven track record of delivering similar results. It's a very compelling argument for why you'd be a great fit for the role.

Connect Personal Passion to Professional Growth

Saying that a particular experience 'lit a fire' in you wonderfully weaves your personal passion into your professional narrative. It shows that you're not just good at what you do, you love what you do. And passion, when channeled right, often leads to innovation and growth - two elements that any employer would value.

Showcase Impact Across Different Roles

When you highlight key achievements from different roles, it paints a picture of consistent success. You're not just boasting about one-off wins, you're showing a pattern of delivering results. And in this case, you didn't just improve numbers; you fostered a culture of continuous improvement, a trait that's key for an Operations Manager.

Express Genuine Excitement

When you say that the 'prospect of contributing to Amazon's global operations excites' you, it's more than just expressing interest in the job. It's about showing genuine enthusiasm for the role and the company, demonstrating that you're not just looking for any job, but this job, at this company.

Offer a Win-Win Scenario

Instead of just stating that you're looking forward to a potential interview, you’re presenting it as an opportunity for them - to discuss how your skills can contribute to their work. This cleverly reframes the conversation as a win-win scenario, making you a more attractive candidate.

Show you know the company

Connect your personal experience with the company's mission to show you're truly interested.

Detail your achievements

Share specific successes to prove your capability in enhancing operations.

Highlight problem-solving skills

Demonstrate how you've tackled challenges to improve business outcomes.

Talk about your passion

Expressing your enthusiasm for the role shows you're a motivated candidate.

Be polite in your closing

A respectful sign-off leaves a positive impression on the reader.

Does writing cover letters feel pointless? Use our AI

Dear Job Seeker, Writing a great cover letter is tough and time-consuming. But every employer asks for one. And if you don't submit one, you'll look like you didn't put enough effort into your application. But here's the good news: our new AI tool can generate a winning cover letter for you in seconds, tailored to each job you apply for. No more staring at a blank page, wondering what to write. Imagine being able to apply to dozens of jobs in the time it used to take you to write one cover letter. With our tool, that's a reality. And more applications mean more chances of landing your dream job. Write me a cover letter It's helped thousands of people speed up their job search. The best part? It's free to try - your first cover letter is on us. Sincerely, The Resume Worded Team

Want to see how the cover letter generator works? See this 30 second video.

Make a personal connection to the company

Sharing your personal experience with the company's products makes your interest feel genuine. This is very appealing.

Demonstrate operations manager success

Highlighting your achievements with clear numbers shows you're capable of making a significant impact. This is exactly what a hiring manager wants to see.

Share your excitement for company values

Expressing excitement about the company’s focus on improvement and innovation suggests a good fit with the company culture. It's a smart way to align with their values.

Close with an invitation to discuss further

Ending your cover letter by inviting further discussion is polite and proactive. It signals you're ready for the next step.

Show your enthusiasm for the company

Talk about why you admire the company. This shows you have done your research and are genuinely interested.

Highlight your achievements in process optimization

Share specific results you have achieved, like reducing stockouts or improving order fulfillment. This shows you can make a real difference.

Express confidence in your fit for the role

Telling us why you're a great match makes it easier for us to see you in the role.

Share your excitement for teamwork

Mentioning your eagerness to work with the team highlights your collaborative spirit.

Close with a forward-looking statement

Ending your letter by looking ahead to contributing to the company's success leaves a positive, proactive impression.

Senior Operations Manager Cover Letter Example

Highlighting relevant skills.

You not only mentioned that you led an initiative to increase operational efficiency by 25%, but you also pointed out how you did it: through data-driven decision-making processes. This is a critical skill in today's data-centric world. By highlighting this skill in context, you're showing the hiring manager that you possess the right skills for the job.

Prove Your Expertise

Implementing a supply chain management system that reduced inventory costs by 30% - that's a big deal. It not only shows you're capable of handling complex systems and processes, but also that you bring valuable expertise in supply chain management. For a Senior Operations Manager role at FedEx, this kind of experience is highly relevant and desirable.

Highlight the Origin of Your Skills

By tracing your skills in critical thinking and agility back to a specific project early in your career, you're not just listing out your abilities. You're telling a story about how you acquired them, making your skills more credible and memorable.

Align Accomplishments with Company Values

Sharing an achievement in sustainability at Google, a company known for its green initiatives, shows you don't just understand their values but have already acted on them. Sure, it's a proud moment for you, but it also signals to Google that you're already aligned with their vision.

Connect Professional Aspirations with Company Mission

When you say that Google's commitment aligns with your professional values, you're not just echoing their mission statement. You're showing that your aspirations are in sync with theirs. This tells them that you're not just interested in a job — you're interested in their mission.

Show Potential Contribution Using Specific Skills

By expressing your expertise in leveraging technology to enhance operational efficiencies, you're making it crystal clear how you can contribute to Google's success. It's not just a vague promise of contribution, but a specific, plausible plan of action.

Share a personal connection

Mentioning a personal relationship with the company's service makes your interest more genuine.

Showcase leadership and results

Illustrate your leadership through concrete results achieved under your guidance.

Mention your unique approach

Talking about your balance between strategic and detailed focus sets you apart.

Emphasize customer-centric thinking

Highlighting a dedication to customer satisfaction aligns with company values.

Thank the reader

Acknowledging the opportunity to apply enhances your professionalism.

Show your personal connection to the company

When you share your personal story of being a pet owner and a customer, it helps me see your genuine interest in our company. It's good to know you understand what we do from both sides.

Highlight leadership in operations

Talking about how you inspire and motivate teams is very important. Operations need leaders who can guide others to success, not just manage tasks.