How To Set Business Goals (+ Examples for Inspiration)

Updated: March 11, 2024

Published: October 24, 2023

You’re a business owner — the captain of your own ship. But how do you ensure you’re steering your company in the right direction?

Without clear-cut goals and a plan to reach them, you risk setting your sails on the course of dangerous icebergs.

The best way to steer clear of wreckage is to map out exactly where you want your business to go. This is what makes setting business goals so important. If you’re not already using them to guide your ship, then now’s a great time to start.

Table of contents:

- What are business goals?

Why business goals are important

How to set business goals, tips to achieve business goals, business goals examples, what are business goals .

Business goals are the desired outcomes that an organization aims to achieve within a specific time frame. These goals help define the purpose and direction of the company, guiding decision-making and resource allocation. They can be short-term or long-term objectives , aligned with the company’s mission and vision.

Operating a business using your gut and feelings will only get you so far. If you’re looking to build a sustainable company, then you need to set goals in advance and follow through with them.

Here’s what goal setting can do to make your business a success:

- Give your business direction. Business goals align everyone toward a common purpose and ensure all efforts and resources are directed toward achieving specific outcomes.

- Keep everyone motivated to keep pushing forward. Goals provide employees with a sense of purpose and motivation. According to research from BiWorldwide, goal setting makes employees 14.2x more inspired at work and 3.6x more likely to be committed to the organization.

- Create benchmarks to work toward (and above). Goals provide a basis for measuring and evaluating the performance of the organization. They serve as benchmarks to assess progress, identify areas of improvement, and make informed decisions about resource allocation and strategy adjustments .

- Prioritize activities and allocate resources effectively. Goals help you identify the most important initiatives, ensuring that time, money, and effort are invested in activities that align with the overall objectives.

- Make continuous organizational improvements. Goals drive continuous improvement by setting targets for growth and progress. They encourage businesses to constantly evaluate their performance, identify areas for refinement, and implement strategies to enhance efficiency and effectiveness.

Nothing creates solidarity among teams and departments like shared goals. So be sure to get everyone involved to boost camaraderie.

Setting business goals requires careful consideration and planning. By defining specific and measurable targets, you can track progress and make necessary adjustments along the way.

Here are the steps to effectively set business goals.

Step 1: Identify key areas to improve in your business

Start by assessing the current state of your organization. Identify areas that require improvement or growth. This could include increasing revenue, expanding your customer base, improving employee satisfaction, or enhancing product offerings.

Step 2: Choose specific and measurable goals

Setting clear and specific goals is essential. Use the SMART goal framework to ensure your goals are Specific, Measurable, Achievable, Relevant, and Time-bound. For example, instead of setting a vague goal like “increase revenue,” set a specific goal like “increase revenue by 15% in the next quarter.”

Step 3: Prioritize which goals to tackle first

Not all goals are equally important or urgent. Evaluate the impact and feasibility of each goal and prioritize them accordingly. By ranking your goals, you can focus your efforts and resources on the most critical objectives.

Step 4: Break down your goals into smaller milestones

Breaking down each goal into smaller, manageable tasks makes them more attainable. Assign responsibilities and set deadlines for each step. This approach helps track progress and ensures accountability.

Step 5: Decide what your Key Performance Indicators (KPIs) will be

Key Performance Indicators (KPIs) are metrics used to measure progress toward your goals. Set realistic and relevant KPIs that align with your objectives. For example, if your goal is to increase customer acquisition, a relevant KPI could be the number of new customers acquired per month.

Now that you have set your business goals, it’s time to take action and work toward achieving them. Here are some tips to help you stay on track:

1. Write down your action plan

Develop a detailed plan of action for each goal. Identify the necessary resources, strategies, and milestones to achieve them. A well-defined action plan provides a road map for success.

2. Foster a culture that’s goal-oriented

Encourage your employees to embrace and contribute to your goals. Foster a culture that values goal setting and achievement. Recognize and reward individuals or teams that make significant progress toward the goals.

3. Regularly track and evaluate progress

Monitor the progress toward each goal and make adjustments as needed. Use project management tools or software to track and visualize progress. Regularly review and evaluate your performance to ensure you’re on the right track.

4. Seek feedback and adapt

Gather feedback from employees, customers, and stakeholders. Their insights can provide valuable perspectives and help you refine your goals and strategies. Adapt your approach based on feedback to increase your chances of success.

5. Stay focused and motivated (even when you fail)

Staying motivated to achieve goals is difficult, especially when you come up short or fail. But don’t let this set you back. Continue pushing forward with your goals or readjust the direction as needed. Then do whatever you can to avoid distractions so you stay committed to your action plan.

Also, remember to celebrate small wins and milestones along the way to keep your team motivated and engaged.

To provide inspiration, here are some examples of common business goals:

1. Revenue growth

Revenue growth is a business goal that focuses on increasing the overall income generated by the company. Setting a specific target percentage increase in revenue can create a measurable goal to work toward.

Strategies for achieving revenue growth may include:

- Expanding the customer base through targeted marketing campaigns

- Improving customer retention and loyalty

- Upselling or cross-selling to existing customers

- Increasing the average order value by offering premium products or services

Example: A retail company sets a goal to increase its revenue by 10% in the next fiscal year. To achieve this, it implements several strategies, including launching a digital marketing campaign to attract new customers, offering personalized discounts and promotions to encourage repeat purchases, and introducing a premium product line to increase the average order value.

2. Customer acquisition

Customer acquisition focuses on expanding the customer base by attracting new customers to the business. Setting a specific goal for the number of new customers helps businesses track their progress and measure the effectiveness of their marketing efforts.

Strategies for customer acquisition may include:

- Running targeted advertising campaigns

- Implementing referral programs to incentivize existing customers to refer new ones

- Forming strategic partnerships with complementary businesses to reach a wider audience

Example: A software-as-a-service (SaaS) company aims to acquire 1k new customers in the next quarter. To achieve this, it launches a social media marketing campaign targeting its ideal customer profile, offers a referral program where existing customers receive a discount for referring new customers, and forms partnerships with industry influencers to promote its product.

3. Employee development

Employee development goals focus on enhancing the skills and knowledge of employees to improve their performance and contribute to the organization’s growth. By setting goals for employee training and skill development, businesses can create a culture of continuous learning and provide opportunities for career advancement.

Strategies for employee development may include:

- Offering training programs

- Providing mentorship opportunities

- Sponsoring professional certifications

- Creating a career development plan for each employee

Example: A technology company aims to have 80% of its employees complete at least one professional certification within the next year. To achieve this, it offers financial support and study materials for employees interested in obtaining certifications, provides dedicated study time during working hours, and celebrates employees’ achievements upon certification completion.

4. Product development

Product development goals focus on creating and improving products or services to meet customer needs and stay competitive in the market. Setting goals for product development can prioritize your efforts and so you can allocate resources effectively.

Strategies for product development may include:

- Conducting market research to identify customer preferences and trends

- Gathering customer feedback through surveys or focus groups

- Investing in research and development to create new products or enhance existing ones

- Collaborating with customers or industry experts to co-create innovative solutions

Example: An electronics company sets a goal to launch three new product lines within the next year. To achieve this, it conducts market research to identify emerging trends and customer demands, gathers feedback from its target audience through surveys and usability testing, allocates resources to research and development teams for product innovation, and collaborates with external design agencies to create visually appealing and user-friendly products.

5. Social responsibility

Social responsibility goals focus on making a positive impact on society or the environment. These goals go beyond financial success and emphasize the importance of ethical and sustainable business practices. Setting goals for social responsibility allows businesses to align their values with their actions and contribute to causes that resonate with their stakeholders.

Strategies for social responsibility may include:

- Implementing sustainable practices to reduce environmental impact

- Donating a percentage of profits to charitable organizations

- Supporting local communities through volunteer programs

- Promoting diversity and inclusion within the organization

Example: A clothing retailer aims to reduce its carbon footprint by 20% in the next two years. To achieve this, it implements sustainable practices, such as using eco-friendly materials, optimizing packaging to minimize waste, and partnering with ethical manufacturers. It also donates a percentage of its profits to an environmental conservation organization.

Setting and achieving goals is what it takes to be successful in business. By following the steps outlined in this article and incorporating the tips provided, you can effectively set and work toward your goals. Remember to regularly evaluate progress, adapt as necessary, and celebrate milestones along the way.

hbspt.cta._relativeUrls=true;hbspt.cta.load(53, 'ad22bdd9-fd50-4b35-a4f5-7586f5a61a1e', {"useNewLoader":"true","region":"na1"});

What did you think of this article .

Give Feedback

Don't forget to share this post!

Outline your company's sales strategy in one simple, coherent plan.

Powerful and easy-to-use sales software that drives productivity, enables customer connection, and supports growing sales orgs

Business Goals 101: How to Set, Track, and Achieve Your Organization’s Goals with Examples

By Kate Eby | November 7, 2022

- Share on Facebook

- Share on LinkedIn

Link copied

Learning how to set concrete, achievable business goals is critical to your organization’s success. We’ve consulted seasoned experts on how to successfully set and achieve short- and long-term business goals, with examples to help you get started.

Included on this page, you’ll find a list of the different types of business goals , the benefits and challenges of business goal-setting, and examples of short-term and long-term business goals. Plus, find expert tips and compare and contrast business goal-setting frameworks.

What Are Business Goals?

Business goals are the outcomes an organization aims to achieve. They can be broad and long term or specific and short term. Business leaders set goals in order to motivate teams, measure progress, and improve performance.

“Business goals are those that represent a company's overarching mission,” says David Bitton, Co-founder and CMO of DoorLoop . “These goals typically cover the entire business and are vast in scope. They are established so that employees may work toward a common goal. In essence, business goals specify the ‘what’ of a company's purpose and provide teams with a general course to pursue.”

For more resources and information on setting goals, try one of these free goal tracking and setting templates .

Business Goals vs. Business Objectives

Many professionals use the terms business goal and business objective interchangeably. Generally, a business goal is a broad, long-term outcome an organization works toward, while a business objective is a specific and measurable task, project, or initiative.

Think of business objectives as the steps an organization takes toward their broader, long-term goals. In some cases, a business objective might simply be a short-term goal. In most cases, business goals refer to outcomes, while business objectives refer to actionable tasks.

“Business objectives are clear and precise,” says Bitton. “When businesses set out to achieve their business goals, they do so by establishing quantifiable, simply defined, and trackable objectives. Business objectives lay out the ‘how’ in clear, doable steps that lead to the desired result.”

For more information and resources, see this article on the key differences between goals and objectives.

Common Frameworks for Writing Business Goals

Goal-setting frameworks can help you get the most out of your business goals. Common frameworks include SMART, OKR, MBO, BHAG, and KRA. Learning about these goal-setting tools can help you choose the right one for your company.

Here are the common frameworks for writing business goals with examples:

- SMART: SMART goals are specific, measurable, achievable, relevant, and time-bound. This is probably the most popular method for setting goals. Ensuring that your goals meet SMART goal criteria is a tried and true way to increase your chances of success and make progress on even your most ambitious goals. Example SMART Goal: We will increase the revenue from our online store by 5 percent in three months by increasing our sign-up discount from 25 to 30 percent.

- OKR: Another popular approach is to set OKRs, or objectives and key results. In order to use OKRs , a team or individual selects an objective they would like to work toward. Then they select key results , or standardized measurements of success or progress. Example Objective: We aim to increase the sales revenue of our online store. Example Key Result: Make $200,000 in sales revenue from the online store in June.

- MBO: MBO, or management by objectives , is a collaborative goal-setting framework and management technique. When using MBO, managers work with employees to create specific, agreed-upon objectives and develop a plan to achieve them. This framework is excellent for ensuring that everyone is aligned on their goals. Example MBO: This quarter, we aim to decrease patient waiting times by 30 percent.

- BHAG: A BHAG, or a big hairy audacious goal , is an ambitious, possibly unattainable goal. While the idea of setting a BHAG might run contrary to a lot of advice about goal-setting, a BHAG can energize the team by giving everyone a shared purpose. These are best for long-term, visionary business goals. Example BHAG: We want to be the leading digital music service provider globally by 2030.

- KRA: KRAs, or key result areas , refer to a short list of goals that an individual, department, or organization can work toward. KRAs function like a rubric for general progress and to help ensure that the team’s efforts have an optimal impact on the overall health of the business. Example KRA: Increase high-quality sales leads per sales representative.

Use the table below to compare the pros and cons of each goal-setting framework to help you decide which framework will be most useful for your business goals.

Types of Business Goals

A business goal is any goal that helps move an organization toward a desired result. There are many types of business goals, including process goals, development goals, innovation goals, and profitability goals.

Here are some common types of business goals:

- Growth: A growth goal is a goal relating to the size and scope of the company. A growth goal might involve increasing the number of employees, adding new verticals, opening new stores or offices, or generally expanding the impact or market share of a company.

- Process: A process goal , also called a day-to-day goal or an efficiency goal , is a goal to improve the everyday effectiveness of a team or company. A process goal might involve establishing or improving workflows or routines, delegating responsibilities, or improving team skills.

- Problem-Solving: Problem-solving goals address a specific challenge. Problem-solving goals might involve removing an inefficiency, changing policies to accommodate a new law or regulation, or reorienting after an unsuccessful project or initiative.

- Development: A development goal , also called an educational goal , is a goal to develop new skills or expertise, either for your team or for yourself. For example, development goals might include developing a new training module, learning a new coding language, or taking a continuing education class in your field.

- Innovation: An innovation goal is a goal to create new or more reliable products or services. Innovation goals might involve developing a new mobile app, redesigning an existing product, or restructuring to a new business model.

- Profitability: A profitability goal , also called a financial goal , is any goal to improve the financial prospects of a company. Profitability goals might involve increasing revenue, decreasing debt, or growing the company’s shareholder value.

- Sustainability: A s ustainability goal is a goal to either decrease your company’s negative impact on the environment or actively improve the environment through specific initiatives. For example, a sustainability goal might be to decrease a company’s carbon footprint, reduce energy use, or divest from environmentally irresponsible organizations and reinvest in sustainable ones.

- Marketing: A marketing goal , also called a brand goal , is a goal to increase a company’s influence and brand awareness in the market. A marketing goal might be to boost engagement across social media platforms or generate more higher-quality leads.

- Customer Relations: A customer relations goal is a goal to improve customer satisfaction with and trust in your product or services. A customer relations goal might be to decrease customer service wait times, improve customers’ self-reported satisfaction with your products or services, or increase customer loyalty.

- Company Culture: A company culture goal , also called a social goal , is a goal to improve the work environment of your company. A company culture goal might be to improve employee benefits; improve diversity, equity, and inclusion (DEI) across your organization; or create a greater sense of work-life balance among employees.

What Are Business Goal Examples?

Business goal examples are real or hypothetical business goal statements. A business goal example can use any goal-setting framework, such as SMART, OKR, or KRA. Teams and individuals use these examples to guide them in the goal-setting process.

For a comprehensive list of examples by industry and type, check out this collection of business goal examples .

What Are Short-Term Business Goals?

Short-term business goals are measurable objectives that can be completed within hours, days, weeks, or months. Many short-term business goals are smaller objectives that help a company make progress on a longer-term goal.

The first step in setting a short-term business goal is to clarify your long-term goals.

“My practice is to start with an aspirational vision that is the framework for my long-term goals and to compare that ‘better tomorrow’ with the realities of today,” says Morgan Roth, Chief Communication Strategy Officer at EveryLife Foundation for Rare Diseases . “Once that framework of three to five major goals is drafted and I have buy-in, I can think about how we get there. Those will be my short-term goals.”

Bitton recommends using the SMART framework for setting short-term business goals to ensure that your team has structure and that their goals are achievable. “Determine which objectives can be attained in a reasonable amount of time,” she adds. “This will help you stay motivated. Your organization may suffer if you try to squeeze years-long ambitions into a month-long project.”

Short-Term Business Goal Examples

Companies can use short-term business goals to increase profits, implement new policies or initiatives, or improve company culture. We’ve gathered some examples of short-term business goals to help you brainstorm your own goal ideas.

Here are three sample short-term business goals:

- Increase Your Market Share: When companies increase their market share, they increase the percentage of their target audience who chooses their product or service over competitors. This is a good short-term goal for companies that have long-term expansion goals. For example, a local retail business might want to draw new customers from the local community. The business sets a goal of increasing the average number of customers who enter its store from 500 per week to 600 per week within three months. It can meet this goal by launching a local advertising initiative, reducing prices, or expanding its presence on local social media groups. Small business owners can check out this comprehensive guide to learn more about setting productive goals for their small businesses.

- Reduce Paper Waste: All businesses produce waste, but company leaders can take actions to reduce or combat excessive waste. Reducing your company’s paper waste is a good short-term goal for companies that have long-term sustainability goals. For example, a large company’s corporate headquarters is currently producing an average of four pounds of paper waste per employee per day. They set a goal of decreasing this number to two pounds by the end of the current quarter. They can meet this goal by incentivizing or requiring electronic reporting and forms whenever possible.

- Increase Social Media Engagement: High social media engagement is essential for businesses that want to increase brand awareness or attract new customers. This is a good short-term goal for companies with long-term marketing or brand goals. For example, after reviewing a recent study, a natural cosmetics company learns that its target audience is 30 percent more likely to purchase products recommended to them by TikTok influencers, but the company’s social media team only posts sporadically on its TikTok. The company sets a goal of producing and posting two makeup tutorials on TikTok each week for the next three months.

What Are Long-Term Business Goals?

A l ong-term business goal is an ambitious desired outcome for your company that is broad in scope. Long-term business goals might be harder to measure or achieve. They provide a shared direction and motivation for team members.

“Long-term planning is increasingly difficult in our very complex and interconnected world,” says Roth. “Economically, politically, and culturally, we’re seeing sea changes in the way we live and work. Accordingly, it’s important to be thoughtful about long-term goal-setting, but not to the point where concerns stifle creativity and your ‘Big Ideas.’ A helpful strategy I employ is to avoid assumptions. Long-term planning should be based on what you know, not on what you assume will be true in some future state.”

Tip: You can turn most short-term goals into long-term goals by increasing their scope. For example, to turn the “increase market share” goal described above into a long-term goal, you might increase the target weekly customers from 600 to 2,000. This will likely take longer than a few months and might require expanding the store or opening new locations.

Long-Term Business Goal Examples

An organization can use long-term business goals to unify their vision, motivate workers, and prioritize short-term goals. We’ve gathered some examples of long-term business goals to guide you in setting goals for your business.

Here are three sample long-term business goals:

- Increase Total Sales: A common growth profitability goal is to increase sales. An up-and-coming software company might set a long-term goal of increasing their product sales by 75 percent over two years.

- Increase Employee Retention: Companies with high employee retention enjoy many benefits, such as decreased hiring costs, better brand reputation, and a highly skilled workforce. A large corporation with an employee retention rate of 80 percent might set a long-term goal of increasing that retention rate to 90 percent within five years.

- Develop a New Technology: Most companies in the IT sphere rely on innovation goals to stay competitive. A company might set a long-term goal of creating an entirely new AI technology within 10 years.

Challenges of Setting Business Goals

Although setting business goals has few downsides, teams can run into problems. For example, setting business goals that are too ambitious, inflexible, or not in line with the company vision can end up being counterproductive.

Here are some common challenges teams face when setting business goals:

- Having a Narrow Focus: One of the greatest benefits of setting business goals is how doing so can focus your team. That said, this can also be a drawback, as such focus on a single goal can narrow the team’s perspective and make people less able to adapt to change or recognize and seize unexpected opportunities.

- Being Overly Ambitious: It’s important to be ambitious, but some goals are simply too lofty. If a goal is impossible to hit, it can be demoralizing.

- Not Being Ambitious Enough: The opposite problem is when companies are too modest with their goal-setting. Goals should be realistic but challenging. Teams that prioritize the former while ignoring the latter will have problems with motivation and momentum.

- Facing Unexpected Obstacles: If something happens that suddenly derails progress toward a goal, it can be a huge blow to a company. Learn about project risk management to better manage uncertainty in your projects.

- Having Unclear Objectives: Goals that are vague or unquantifiable will not be as effective as clear, measurable goals. Use frameworks such as SMART goals or OKRs to make sure your goals are clear.

- Losing Motivation: Teams can lose sight of their goals over time, especially with long-term goals. Be sure to review and assess progress toward goals regularly to keep your long-term vision front of mind.

Why You Need Business Goals

Every business needs to set clear goals in order to succeed. Business goals provide direction, encourage focus, improve morale, and spur growth. We’ve gathered some common benefits of goal-setting for your business.

Here are some benefits you can expect from setting business goals:

- More Clarity: Business goals ensure that everyone is moving toward a determined end point. Companies with clear business goals have teams that agree on what is important and what everyone should be working toward.

- Increased Focus: Business goals encourage focus, which improves performance and increases productivity.

- Faster Growth: Business goals help companies expand and thrive. “Setting goals and objectives for your business will help you grow it more quickly,” says Bitton. “Your potential for growth increases as you consistently accomplish your goals and objectives.”

- Improved Morale: Everyone is happier when they are working toward a tangible goal. Companies with clear business goals have employees that are more motivated and fulfilled at work. Plus, measuring progress toward specific goals makes it easier to notice and acknowledge everyone’s successes.

- More Accountability: Having tangible goals means that everyone can see whether or not their work is effective at making progress toward those goals.

- Better Decision-Making: Business goals help teams prioritize tasks and make tough decisions. “You gain perspective on your entire business, which makes it easier for you to make smart decisions,” says Bitton. “You are forming a clear vision for the direction you want your business to go, which facilitates the efficient distribution of resources, the development of strategies, and the prioritization of tasks.”

Improve Your Goal-Setting with Real-Time Work Management in Smartsheet

Empower your people to go above and beyond with a flexible platform designed to match the needs of your team — and adapt as those needs change.

The Smartsheet platform makes it easy to plan, capture, manage, and report on work from anywhere, helping your team be more effective and get more done. Report on key metrics and get real-time visibility into work as it happens with roll-up reports, dashboards, and automated workflows built to keep your team connected and informed.

When teams have clarity into the work getting done, there’s no telling how much more they can accomplish in the same amount of time. Try Smartsheet for free, today.

Discover why over 90% of Fortune 100 companies trust Smartsheet to get work done.

How to set up and achieve long term goals for a business

What are long-term goals for business?

Long-term goals for business are the high-level goals of your strategy that you aim to achieve in the next 3-5 years or even longer. They are the objectives that, once reached, bring you closer to your vision.

They are the milestones for your vision.

They tend to be resilient to environmental changes like technological, political and others. Long-term goals determine the direction of your company and solidify your strategy regarding your position in the market and the industry. In other words, they outline the high-level objectives you choose to accomplish to bring your vision to life.

Why it’s important to set long-term goals

They provide clarity ..

A business with weak or non-existent long-term goals is like a leaf in the wind.

It moves in no particular direction and is subject to every and any change in the environment. It jumps from trend to trend without understanding what causes them, trying to get as much benefit out of them as possible. Sometimes it succeeds, others not so much. As a result, its performance is a roller coaster and its future unpredictable and uncertain. These kinds of businesses move fast towards nowhere.

A business with no long-term goals is in reactive mode .

On the other hand , organizations with long-term goals deriving from their vision have a more steady course. They have clarity on what they wish to become in the next 3-5 years, which guides their decisions. It’s easier for them to spot meaningful trends and take advantage of them in the short term to succeed in the longer term.

Clarity in the organization’s future state, when combined with a concise view of its current state , is a powerful tool. It enables an accurate gap analysis and the grounding of the strategy in reality.

A business with solid and aligned long-term goals is in proactive mode .

How short-term and long-term goals differ

Long-term goals differ from short-term goals in four key traits:

- Short-term goals are malleable .

- Short-term goals are specific .

- Short-term goals are measurable .

- Short-term goals are sacrificable .

Short-term goals change often. As they should. They correlate to the tactics you choose to pursue your strategic objectives. And your tactics change when the environmental circumstances change, e.g., your competitors launched a new product, a global pandemic came out of nowhere, your country leaves a state union , or a new tech disrupts your industry. All of these changes force you to adapt your short-term expectations and tactics. Your long-term goals are more resilient to these changes.

Short-term goals love specificity. This is goal setting 101. Remove ambiguity and make sure that everybody interprets the goals the same way. Make your language simple and your description longer if you have to. Clarity in goals informs decisions. Of course, long-term goals should be clear, as well, but they don’t have to be so specific.

Short-term goals have numbers in them. They are not metrics or KPIs because they’re lagging indicators of your progress. But they are indicators nonetheless. They inform you whether you and your people did a good job to achieve them. Long-term goals don’t need numbers if they don’t make sense. For example, “Dominate our category” could be accompanied by a number like “Own 70% of the market”, but that doesn’t exactly sum up what “dominating a category” really is.

Short-term goals are sacrificed for the company’s greater good. We’re past the time where quarterly numbers are the holy grail of strategy. Leadership with a clear vision recognizes that sometimes you have to make short-term sacrifices to achieve long-term success. It’s how you build sustainable and stable growth. The reverse is what creates soaring short-term results but destroys the culture and leads to ethical fading.

How long are short-term and long-term goals

The scale is relative.

A colossus like Amazon can’t really keep up and survive with a strategy shorter than 3 years . The bigger the organization (and its market cap), the longer the span of its long-term goals. Planning for so long ahead allows the company to manage its resources efficiently and direct its effort towards the most promising big move.

In his book “Invent & Wander: The Collected Writings of Jeff Bezos,” Jeff Bezos says that each quarter is baked three years earlier . Not three months. Not three quarters. Three years. Which means that the numbers of the latest quarter indicate the quality of the company’s 3- year-old strategy. And it makes sense. It’s impossible to coordinate over a million employees if you change the company's direction with every small trend you spot.

Of course, that doesn’t mean the strategy doesn’t adapt to environmental changes.

Complacency is the enterprise killer . Large organizations might be more resilient to threats, but they can become irrelevant very fast, remember Blockbuster and Kodak. However, with size comes one huge advantage. Data. Large organizations have access to huge amounts of data that can generate market insights, spot trends and almost “predict the future.”

Short-term and medium-term goals are decided based on those findings. Due to their dependence on environmental conditions, short-term goals can’t be yearly . Even longer than quarterly is stretching them. In a time of a crisis, short-term goals could be as short as daily and in more peaceful circumstances as long as quarterly.

Long-term goals examples

The further you look into the future, the more uncertain it becomes. The closer your milestones are to your vision, the less specific they become.

Let’s take, for example, The Walt Disney Company . Disney’s vision statement is:

“To be one of the world’s leading producers and providers of entertainment and information.” When Bob Iger took over as Disney’s CEO, his strategy was summed up in three priorities, 3 long-term goals :

- Create content of the highest quality

- Adopt cutting-edge technology to create content & connect with the customers

- Expand globally

These goals are specific enough to guide the decisions of everyone inside the company and are vague enough for everyone to interpret them differently. In other words, they are contextualizing the content of the rest of the strategy.

Other long-term goals examples are:

- Dominate our category

- Create a community-like culture

- Lead the sustainability transformation in our industry

- Create the most comfortable/cheapest/easiest to use [product]

- Digitize our processes

Short-term goals examples

Short-term goals are very specific.

Each department, team and individual has its own short-term goals to meet. What’s important is to have all of them aligned, some shared between teams and people and none isolated. Choosing short-term goals is the last step of your strategy’s implementation and should derive naturally from your strategic priorities.

Here is a list of short-term goals:

- Increase our revenue by 15% by the end of Q1 owned by Jane Doe.

- Reduce safety incidents by 70% by the end of Q1 owned by John Doe.

- Increase customer retention by 30% by the end of Q2 owned by John Doe.

- Hire 5 new salespeople by the end of the month owned by Jane Doe.

- Increase ad conversion by 10% by the end of the next month owned by Jane Doe.

How to set long-term goals

Long-term goals have 3 important components:

- Duration (NOT deadline)

- Specificity to dictate choices

- They are memorable

They don’t have a specific deadline. They have an estimated duration. You don’t “Dominate your category” by Dec 31, 2025. You “Dominate your category” in the next 3 years. If in 3 years you haven’t achieved your goal, then something went wrong. That’s how you should think of your long-term deadline, not as a hard date but as an estimated duration.

They dictate choices. Long-term goals outline the company’s strategy and inform every employee’s decision-making process. Ideally, when a team leader needs to make a decision, crucial or not, they can easily align it with the company’s strategy simply by visiting the long-term goals. That’s why they can’t be overly specific because they will only inform certain types of decisions and be useful to only a limited part of the organization. Thus, creating a big risk of internal misalignment.

They are easy to remember. If your people need to check the company’s long-term priorities every time they make a decision, they won’t. Make sure everyone understands and is on board with your priorities by simply making them memorable. In the end, you want the priorities to provide context, not represent all of your strategy’s details.

Benchmark the duration of your goals externally

Take as much guessing as possible out of the process. Have a hard look at your industry’s history and how long it took certain players to achieve their long-term aspirations. Find out what were their strengths, weaknesses and mistakes . Contrast them to yours and then make an educated estimation of your goal’s duration.

Do better than “best”

Shy away from generic goals like “be the best/first/most innovative.” Nobody perceives these the same way. For example, specify your ideal customer so your people know who NOT to target. Specify your product’s niche , e.g., “perfect scale models” instead of “just toys.” In essence, provide a context to decisions that will dictate a clear set of choices on every organizational level.

Write them for 5-year-olds

If a young child can’t understand your long-term goals, chances are your people will have a hard time remembering them. Simplify the language, avoid jargon, use verbs and be specific in your adjectives . Go beyond 3 goals and you risk giving your people contradicting priorities. Clarity unifies collective effort towards one direction .

How to achieve long-term goals in business

With shorter-term goals.

When you write your strategic plan , start from the end and work your way backward from your vision towards your current state. Here’s how to think about your plan:

- Your vision is your destination.

- Your long-term goals are your milestones.

- Your shorter-term goals are your odometer.

Your strategic plan also contains your Focus Areas and your strategic objectives . They break down your direction even further.

Starting with the end in mind gives your shorter-term goals a predictive power

So basically, your strategic plan works like a roadmap towards your long-term goals. Here’s how to think about tracking your progress: if you complete all of your strategic objectives, will you have achieved your long-term goals? If you haven’t achieved at least an 80% progress towards them, your tracking is off. You need to revisit your strategic objectives.

This tracking process cascades from the top of the strategic plan to the bottom. Check out how Cascade brings this strategic model to life and aligns your people’s day-to-day work with your company’s vision as a goal management software .

Popular articles

Viva Goals Vs. Cascade: Goal Management Vs. Strategy Execution

What Is A Maturity Model? Overview, Examples + Free Assessment

How To Implement The Balanced Scorecard Framework (With Examples)

The Best Management Reporting Software For Strategy Officers (2024 Guide)

Your toolkit for strategy success.

- Business Essentials

- Leadership & Management

- Credential of Leadership, Impact, and Management in Business (CLIMB)

- Entrepreneurship & Innovation

- Digital Transformation

- Finance & Accounting

- Business in Society

- For Organizations

- Support Portal

- Media Coverage

- Founding Donors

- Leadership Team

- Harvard Business School →

- HBS Online →

- Business Insights →

Business Insights

Harvard Business School Online's Business Insights Blog provides the career insights you need to achieve your goals and gain confidence in your business skills.

- Career Development

- Communication

- Decision-Making

- Earning Your MBA

- Negotiation

- News & Events

- Productivity

- Staff Spotlight

- Student Profiles

- Work-Life Balance

- AI Essentials for Business

- Alternative Investments

- Business Analytics

- Business Strategy

- Business and Climate Change

- Design Thinking and Innovation

- Digital Marketing Strategy

- Disruptive Strategy

- Economics for Managers

- Entrepreneurship Essentials

- Financial Accounting

- Global Business

- Launching Tech Ventures

- Leadership Principles

- Leadership, Ethics, and Corporate Accountability

- Leading Change and Organizational Renewal

- Leading with Finance

- Management Essentials

- Negotiation Mastery

- Organizational Leadership

- Power and Influence for Positive Impact

- Strategy Execution

- Sustainable Business Strategy

- Sustainable Investing

- Winning with Digital Platforms

How to Set Strategic Planning Goals

- 29 Oct 2020

In an ever-changing business world, it’s imperative to have strategic goals and a plan to guide organizational efforts. Yet, crafting strategic goals can be a daunting task. How do you decide which goals are vital to your company? Which ones are actionable and measurable? Which goals to prioritize?

To help you answer these questions, here’s a breakdown of what strategic planning is, what characterizes strategic goals, and how to select organizational goals to pursue.

Access your free e-book today.

What Is Strategic Planning?

Strategic planning is the ongoing organizational process of using available knowledge to document a business's intended direction. This process is used to prioritize efforts, effectively allocate resources, align shareholders and employees, and ensure organizational goals are backed by data and sound reasoning.

Research in the Harvard Business Review cautions against getting locked into your strategic plan and forgetting that strategy involves inherent risk and discomfort. A good strategic plan evolves and shifts as opportunities and threats arise.

“Most people think of strategy as an event, but that’s not the way the world works,” says Harvard Business School Professor Clayton Christensen in the online course Disruptive Strategy . “When we run into unanticipated opportunities and threats, we have to respond. Sometimes we respond successfully; sometimes we don’t. But most strategies develop through this process. More often than not, the strategy that leads to success emerges through a process that’s at work 24/7 in almost every industry."

Related: 5 Tips for Formulating a Successful Strategy

4 Characteristics of Strategic Goals

To craft a strategic plan for your organization, you first need to determine the goals you’re trying to reach. Strategic goals are an organization’s measurable objectives that are indicative of its long-term vision.

Here are four characteristics of strategic goals to keep in mind when setting them for your organization.

1. Purpose-Driven

The starting point for crafting strategic goals is asking yourself what your company’s purpose and values are . What are you striving for, and why is it important to set these objectives? Let the answers to these questions guide the development of your organization’s strategic goals.

“You don’t have to leave your values at the door when you come to work,” says HBS Professor Rebecca Henderson in the online course Sustainable Business Strategy .

Henderson, whose work focuses on reimagining capitalism for a just and sustainable world, also explains that leading with purpose can drive business performance.

“Adopting a purpose will not hurt your performance if you do it authentically and well,” Henderson says in a lecture streamed via Facebook Live . “If you’re able to link your purpose to the strategic vision of the company in a way that really gets people aligned and facing in the right direction, then you have the possibility of outperforming your competitors.”

Related: 5 Examples of Successful Sustainability Initiatives

2. Long-Term and Forward-Focused

While strategic goals are the long-term objectives of your organization, operational goals are the daily milestones that need to be reached to achieve them. When setting strategic goals, think of your company’s values and long-term vision, and ensure you’re not confusing strategic and operational goals.

For instance, your organization’s goal could be to create a new marketing strategy; however, this is an operational goal in service of a long-term vision. The strategic goal, in this case, could be breaking into a new market segment, to which the creation of a new marketing strategy would contribute.

Keep a forward-focused vision to ensure you’re setting challenging objectives that can have a lasting impact on your organization.

3. Actionable

Strong strategic goals are not only long-term and forward-focused—they’re actionable. If there aren’t operational goals that your team can complete to reach the strategic goal, your organization is better off spending time and resources elsewhere.

When formulating strategic goals, think about the operational goals that fall under them. Do they make up an action plan your team can take to achieve your organization’s objective? If so, the goal could be a worthwhile endeavor for your business.

4. Measurable

When crafting strategic goals, it’s important to define how progress and success will be measured.

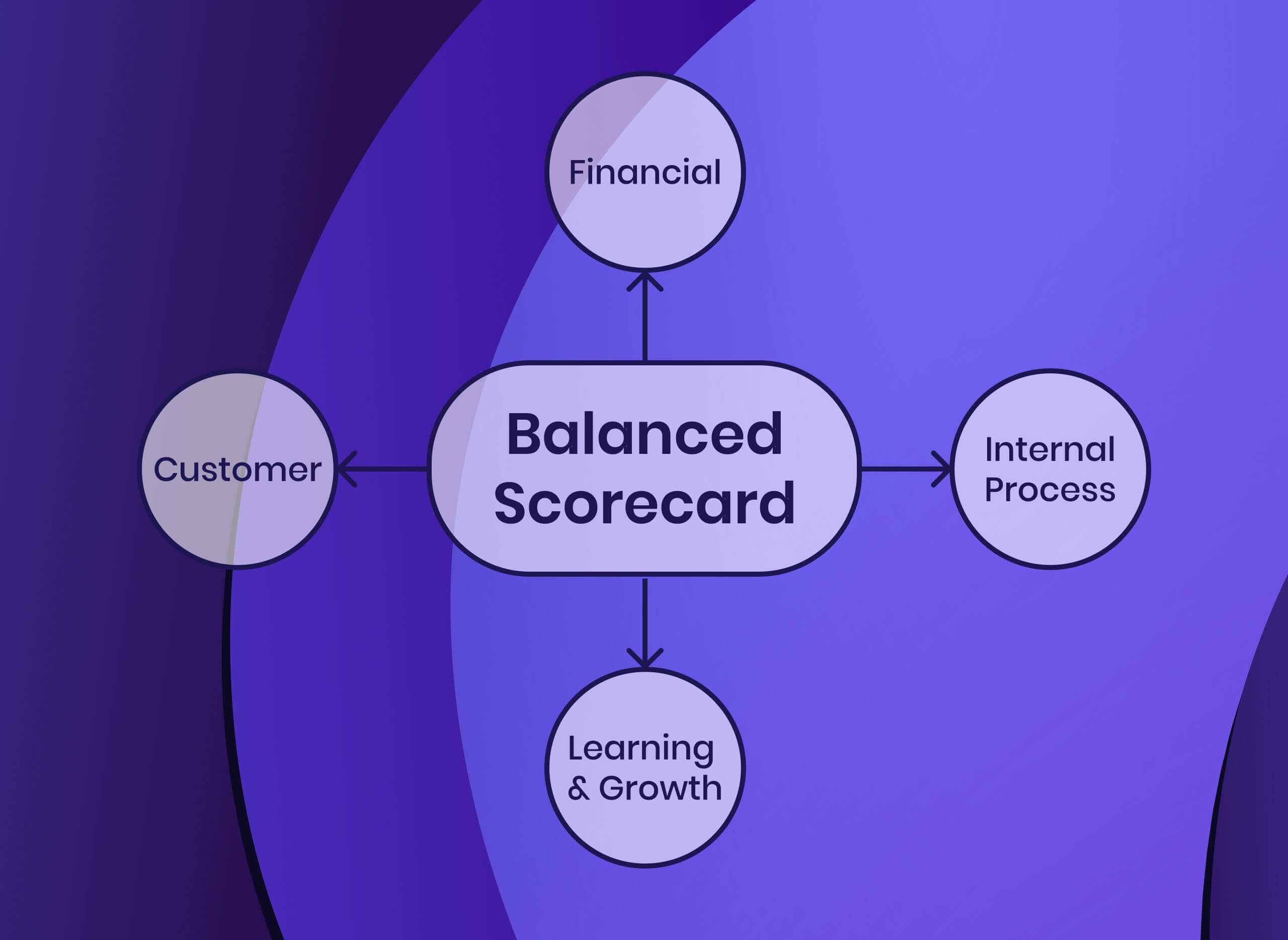

According to the online course Strategy Execution , an effective tool you can use to create measurable goals is a balanced scorecard —a tool to help you track and measure non-financial variables.

“The balanced scorecard combines the traditional financial perspective with additional perspectives that focus on customers, internal business processes, and learning and development,” says HBS Professor Robert Simons in the online course Strategy Execution . “These additional perspectives help businesses measure all the activities essential to creating value.”

The four perspectives are:

- Internal business processes

- Learning and growth

The most important element of a balanced scorecard is its alignment with your business strategy.

“Ask yourself,” Simons says, “‘If I picked up a scorecard and examined the measures on it, could I infer what the business's strategy was? If you've designed measures well, the answer should be yes.”

Related: A Manager’s Guide to Successful Strategy Implementation

Strategic Goal Examples

Whatever your business goals and objectives , they must have all four of the characteristics listed above.

For instance, the goal “become a household name” is valid but vague. Consider the intended timeframe to reach this goal and how you’ll operationally define “a household name.” The method of obtaining data must also be taken into account.

An appropriate revision to the original goal could be: “Increase brand recognition by 80 percent among surveyed Americans by 2030.” By setting a more specific goal, you can better equip your organization to reach it and ensure that employees and shareholders have a clear definition of success and how it will be measured.

If your organization is focused on becoming more sustainable and eco-conscious, you may need to assess your strategic goals. For example, you may have a goal of becoming a carbon neutral company, but without defining a realistic timeline and baseline for this initiative, the probability of failure is much higher.

A stronger goal might be: “Implement a comprehensive carbon neutrality strategy by 2030.” From there, you can determine the operational goals that will make this strategic goal possible.

No matter what goal you choose to pursue, it’s important to avoid those that lack clarity, detail, specific targets or timeframes, or clear parameters for success. Without these specific elements in place, you’ll have a difficult time making your goals actionable and measurable.

Prioritizing Strategic Goals

Once you’ve identified several strategic goals, determine which are worth pursuing. This can be a lengthy process, especially if other decision-makers have differing priorities and opinions.

To set the stage, ensure everyone is aware of the purpose behind each strategic goal. This calls back to Henderson’s point that employees’ alignment on purpose can set your organization up to outperform its competitors.

Calculate Anticipated ROI

Next, calculate the estimated return on investment (ROI) of the operational goals tied to each strategic objective. For example, if the strategic goal is “reach carbon-neutral status by 2030,” you need to break that down into actionable sub-tasks—such as “determine how much CO2 our company produces each year” and “craft a marketing and public relations strategy”—and calculate the expected cost and return for each.

The ROI formula is typically written as:

ROI = (Net Profit / Cost of Investment) x 100

In project management, the formula uses slightly different terms:

ROI = [(Financial Value - Project Cost) / Project Cost] x 100

An estimate can be a valuable piece of information when deciding which goals to pursue. Although not all strategic goals need to yield a high return on investment, it’s in your best interest to calculate each objective's anticipated ROI so you can compare them.

Consider Current Events

Finally, when deciding which strategic goal to prioritize, the importance of the present moment can’t be overlooked. What’s happening in the world that could impact the timeliness of each goal?

For example, the coronavirus (COVID-19) pandemic and the ever-intensifying climate change crisis have impacted many organizations’ strategic goals in 2020. Often, the goals that are timely and pressing are those that earn priority.

Learn to Plan Strategic Goals

As you set and prioritize strategic goals, remember that your strategy should always be evolving. As circumstances and challenges shift, so must your organizational strategy.

If you lead with purpose, a measurable and actionable vision, and an awareness of current events, you can set strategic goals worth striving for.

Do you want to learn more about strategic planning? Explore our online strategy courses and download our free flowchart to determine which is right for you and your goals.

This post was updated on November 16, 2023. It was originally published on October 29, 2020.

About the Author

What Are Long-Term Goals? (+50 Examples & Tips to Achieve Them)

Learn all you need to know about setting long-term goals and how to achieve them. Plus, a list of 50 long-term goal examples you can use as inspiration.

Setting long-term goals is important if you want to succeed in your life and career.

In fact, over 1,000 studies have found that setting lofty, specific goals is linked to higher levels of performance, motivation, and persistence.

But what exactly are long-term goals? How can you set them? And most importantly, how can you achieve them?

Let’s look at long-term goals, why they’re important, and how you can make them a reality. We’ll also give you a list of 50 long-term goal examples so you can be inspired to aim high when setting your goals.

What are long-term goals?

Put simply, a long-term goal is an objective you want to achieve in the future — but one that’ll take a fair amount of effort and time. They’re not something you can achieve in a week or even a year; long-term goals are big goals that concern your health, finances, or career.

To achieve long-term goals, you need to:

- Plan carefully to make sure each goal is realistic and achievable

- Include different milestones to ensure progression

- Consistently put in the work (even if the results are taking longer than expected)

- Remain focused and accountable throughout the process

Difference between long and short-term goals

While both long and short-term goals have end objectives, their scales and the time frames required to achieve them are different.

Short-term goals can take anywhere from a few days to a year to complete, whereas long-term goals can take five years or longer.

Long-term goals are also often made up of short-term goals or smaller milestones that help you stay accountable and measure your progress.

For example, if your long-term goal is to buy a house, you may have several short-term goals to help you afford the property, such as getting a promotion, investing in stock, or taking out a loan.

Since long-term goals are achieved over a long period, they’re more flexible than short-term goals. This is because circumstances that are out of your control (such as inflation when saving to buy a house) may change, and you may need to adjust your overall objective or timeframe as a result.

On the other hand, short-term goals are more specific and often list specific tasks that need to be completed over relatively short periods.

Why is it important to set long-term goals?

Without setting long-term goals, it’s impossible to know where you want to go — let alone how you’ll get there.

In 2018, John Doeer, an American investor with a net worth of over $4 billion , spoke at a TED conference about the importance of goal setting. He went so far as to say that the “secret” to success is setting the right goals.

Not only do long-term goals give you a long-term vision, but they also inspire and motivate you to take deliberate, small actions to help meet them.

They help you stay focused and “keep your eyes on the prize.” As a result, you’ll be better able to organize your time, projects, and resources to achieve the things you truly want.

According to Positive Psychology , setting goals can also help trigger new behaviors that’ll help you gain momentum in your life.

Long-term goal setting can even promote a sense of self-mastery since your goals will push you to step out of your comfort zone and do things you never thought you were capable of.

Examples of long-term goals

You can set different types of goals for the business, career, personal, and financial areas of your life.

Here are some examples of what these goals could look like:

Long-term business goals

- Grow a successful business

- Reach a monthly revenue of X amount

- Expand your business to a new country or region

- Hire a skilled team of workers

- Travel the world while managing your company remotely

- Rebrand your business

- Increase employee satisfaction and retention

- Leave a legacy

- Develop a personal brand

- Acquire a competitor company

- Grow your customer base to X amount

- Increase shareholder value

- Become a public speaker

Long-term career goals

- Find your dream job

- Improve your work-life balance

- Master a new job skill

- Become a company executive

- Work internationally

- Retire from full-time work

- Shift to a new career path

- Experience career stability

- Achieve a salary of X amount

- Expand your professional network

- Mentor other employees

- Pursue further education

- Become an expert in your industry

Want to set better goals for your career? Read our ultimate guide to setting professional goals .

Long-term personal goals

- Buy a house

- Live abroad

- Go on your dream vacation (such as a two-week trip to Hawaii)

- Achieve your ultimate fitness level and weight

- Learn to cook like a chef

- Complete a difficult event, such as a marathon

- Have or adopt a child

- Maintain your ideal weight

- Find your life partner

- Become a better parent

- Become a better spouse

- Emigrate to a different country

- Learn to play an instrument

Long-term financial goals

- Become a millionaire

- Improve your credit score

- Pay off your large debts

- Grow your savings account balance

- Invest in something big

- Build an emergency fund

- Saving for a college fund for your kids

- Pay off your car

- Fund your retirement

- Invest money in stock or properties to get X amount of return on investment

- Become financially independent

According to a 2022 Hearts and Wallets research report, long-term financial goals matter to 82% of American households.

How to set and achieve long-term goals

Setting long-term goals can be tricky and sometimes even overwhelming. Here are some general guidelines you can follow to make it easier:

1. Think of where you want to be in 10 years

You need to visualize your “perfect” future before you even think about creating long-term goals.

Remember that long-term goals require commitment and take several years to achieve. So, you don’t want to end up setting a goal that doesn’t fit into your life or business.

If you’re setting a long-term personal or career goal, it needs to align with your values and be something that matters to you. On the other hand, if you’re setting a business goal, ensure that it aligns with your company’s mission, vision, and values.

Having something to aim for that’ll really impact your life or business will help you stick to your goal — even during uncertain times.

2. Write SMART goals

The SMART goals framework is a popular method used for setting long-term goals. It focuses on helping you set goals that aren’t only suited to you and what you want but that are also realistic and achievable.

SMART stands for specific, measurable, attainable, relevant, and time-bound.

When setting SMART goals, ask yourself the following questions:

- Specific: What exactly is it that you want to achieve? Make the goal as specific as possible. For example, if you’re setting a financial goal, include a specific monetary amount.

- Measurable: How will you know whether you’ve achieved your goal? Set up key performance indicators that’ll make it clear whether your goal has been met or not.

- Attainable: Is your goal possible to achieve? Make sure it’s realistic and can be reached within the specified time frame.

- Relevant: Does your goal contribute to your overall personal, career, or business growth? Ensure you set a goal that fits into your dream life or career. It needs to be focused on what you truly desire.

- Time-bound: When do you want to achieve your goal? Choose a day you can use as a deadline. The more specific with it you get, the better.

3. Reverse-engineer your goal

Long-term goals can be overwhelming since they’re far more complex than short-term goals. They leave room for you to become demotivated since they can sometimes seem unattainable.

That’s why they should be broken down into short-term, bite-sized, less intimidating goals.

In other words, you need to create a more manageable action plan.

You can do this by reverse-engineering the objective. Start at the end and work backward to determine the smaller tasks that need to be completed for you to attain your ultimate goal.

Like long-term goals, each short-term goal should be based on the SMART framework.

For example, if your long-term goal is to grow a successful business, your short-term goals might include things like the following:

- Writing a business plan

- Gaining funding

- Opening a business bank account

- Hiring your first employee

4. Prioritize your goals

You can use a planning system such as Motion to prioritize your tasks and manage your schedule — and in doing so, make it easier to achieve your long-term goals.

Motion allows you to use time-blocking to set aside a specific amount of time to complete different tasks. This helps you to be more productive and get the work done!

With Motion, you can also merge your personal and professional goals — making it possible for you to work on home and work responsibilities on the same day without feeling overwhelmed.

You can also move tasks around whenever emergencies arise so you don’t forget about them — and rest assured that your tasks will be completed no matter what.

5. Make a plan to track your progress

This is where the “measurable” part of your SMART goal comes in. You need to make sure that your long-term and short-term goals are measurable.

For example, if you have a short-term goal of improving your networking and communication abilities, you could measure it through the tasks you complete.

Thus, your tasks may look something like this:

- Reaching out to three new people in your industry per day via email

- Taking a one-week communication course

- Going to a networking event

- Communicating more during work meetings

Completing each of these subtasks with the help of a tool like Motion could help you move toward completing your bigger goal. You can set the urgency of each task, its due date, and much more.

6. Be willing to make changes

As mentioned above, unexpected obstacles sometimes arise. And often, these obstacles are out of your control.

It’s important to remember that things change — and that’s okay.

When you’re aiming for a long-term goal, it’s completely normal for things to occur that knock you off track or for your long-term goal to shift. After all, a lot can happen in 5–10 years!

Rather than becoming demotivated when things change, maintain a mindset of flexibility. If you focus too much on a fixed outcome, you might miss out on other opportunities.

For example, if you’ve set a goal to emigrate to a specific country, but that country’s financial state declines dramatically — no longer making it a viable option — be willing to shift your goal. Look into other countries that could be better options.

Ready to set ambitious long-term goals?

Now that you know how to set your long-term goals, you can get to work setting business and personal goals that resonate with you and your dream life.

Setting these goals may take some soul-searching, but once you have them in mind, you can start working on your plan to get there.

Be sure to use a to-do list app , as this will help you measure your progress toward your goals much faster.

Related articles

The Secrets to Effective Sprint Planning

6 Best AI Calendar Assistants for Easy Organization

Understanding the Sprint Backlog and How to Use It

Put motion to the test., tech and media companies are talking about motion.

11 Tips for Creating a Long-Term Strategic Plan

7 min. read

Updated October 29, 2023

Strategic planning is a management tool that guides your business to better performance and long-term success.

Working with a plan will focus your efforts, unify your team in a single direction, and help guide you through tough business decisions. A strategic plan requires you to define your goals, and in defining them, enables you to achieve them—a huge competitive advantage.

In this article, we’ll discuss 11 essentials for creating a thorough and effective strategic plan. Each tip is a critical stepping stone in leading your business toward your goals.

- 1. Define your company vision

You should be able to define your company vision in 100 words. Develop this statement and make it publically available to both employees and customers.

This statement should answer the key questions that drive your business: Where is your company headed? What do you want your company to be? If you don’t know the answer to these questions off the top of your head, then you have some thinking to do! If you have the answers in your head, but not on paper—get writing.

If you have them written down, congrats! You’ve completed the first and most critical step in creating a long-term strategic plan.

- 2. Define your personal vision

While your personal vision is just as important to your strategic plan, it does not need to be shared with your team and customers.

Your personal vision should incorporate what you want your business to bring to your life—whether that’s enormous growth, early retirement, or simply more time to spend with family and friends.

Aligning your personal vision with your company vision is key to achieving your personal and professional goals. Just as with your company vision, have your personal vision written down in a 100-word statement. Know that statement inside and out and keep it at the forefront of your decision making.

- 3. Know your business

Conduct a SWOT (strengths, weaknesses, opportunities, and threats) analysis. By knowing where your business is now, you can make more informed predictions for how it can grow.

Questions such as “Why is this business important?” and “What does this business do best?” are a great place to start. A SWOT analysis can also help you plan for making improvements.

Questions such as “What needs improvement?” and “What more could the business be doing?” can help guide your strategic plan in a way that closes gaps and opens up opportunities.

For more on completing a SWOT analysis, see our SWOT analysis guide.

Brought to you by

Create a professional business plan

Using ai and step-by-step instructions.

Secure funding

Validate ideas

Build a strategy

- 4. Establish short-term goals

Short-term goals should include everything you (realistically) want to achieve over the next 36 months.

Goals should be “S.M.A.R.T.” (specific, measurable, actionable, reasonable, and timely).

An example of S.M.A.R.T. goals include “building out a new product or service within the next year” or “increasing net profit by 2 percent in ten months.” If you’ve already conducted a SWOT analysis, you should have an idea of what your business can reasonably achieve over a specified period of time.

- 5. Outline strategies

Strategies are the steps you’ll take to meet your short-term goals. If the short term goal is “build out a new product or service,” the strategies might be:

- Researching competitor offerings

- Getting in touch with vendors and suppliers

- Formulating a development plan

- Outlining a marketing and sales plan for the new offering

- 6. Create an action plan

An action plan is an essential part of the business planning and strategy development process. The best analysis, in-depth market research, and creative strategizing are pointless unless they lead to action.

An action plan needs to be a working document; it must be easy to change and update. But, must also be specific about what you’re doing, when you will do it, who will be accountable, what resources will be needed, and how that action will be measured.

Action plans put a process to your strategies. Using the previous example, an action plan might be: “CMO develops competitor research packet for new offerings by 9/1. Review packet with the executive team by 9/15.”

When The Alternative Board, Bradford West Director Andrew Hartley was responsible for designing and delivering a three year, $10m environmental business support program, a full and detailed action plan was required for funding.

“That action plan allowed me to 1.) manage and measure the evolving program, 2.) ensure resources and staff were where they needed to be, and 3.) track whether the design of the program was working and delivering the level of results we were contracted to deliver,” says Hartley.

“Even I was surprised about how helpful that action plan was,” he says. “I cannot image approaching any significant project or business without one.”

- 7. Foster strategic communication

To align your team, you must communicate strategically. Results-driven communication focuses conversations and cuts out excessive meetings. Every communication should be rooted in a specific goal.

Include the how, where, when, and most importantly why every time you deliver instructions, feedback, updates, and so on.

- 8. Review and modify regularly

Check in regularly to make sure you’re progressing toward your goals. A weekly review of your goals, strategies, and action plans can help you see if you need to make any modifications.

Schedule time in your calendar for this. Weekly check-ins allow you to reassess your plan in light of any progress, setbacks, or changes.

- 9. Hold yourself accountable

Having a business coach or mentor is great for this. If you have a hard time sticking to your plans, you’ll have an equally hard time meeting your goals.

According to The Alternative Board’s September 2015 Business Pulse Survey, the number one reason business owners choose to work with mentors is accountability.

“Having a close—but not too close—space for advice and accountability is really valuable,” says TAB Member Scott Lininger, CEO of Bitsbox. “Someone who is too close to your business (such as board members) often have a perspective that’s too similar to your own. Over time, your coach comes to know your team, your product, and your business, and they help you work through all kinds of challenges in a way that’s unique.”

“All too often I find that leaders accept underperformance against their strategic plan too easily,” adds Hartley. “A coach can rekindle the resolve and ambition of the leader, resulting in a recovery of lost margins, sales, or output.”

According to Hartley, a coach can build accountability by questioning what’s working, making sure everything’s on track, pointing out areas of underperformance, and asking what corrective action needs to be pursued.

- 10. Be adaptable

Remember: You can’t plan for everything. Just as challenges will arrive, so too will opportunities, and you must be ready at a moment’s notice to amend your plan. Weekly reviews will help enormously with this.

“A strategic plan will likely need to be changed very soon after approval because nobody can accurately predict anything but the very near term future,” says Jim Morris, owner and President of The Alternative Board, Tennessee Valley. “You stay adaptable by monitoring the plan every day. The wise leader will be constantly looking for opportunities to exceed the strategic plan by being opportunistic, creative, and by exploiting weaknesses in the competitive market.”

By doing this, Morris was able to exceed forecast results of every strategic plan he ever approved. “The times when I needed to be flexible were when we met strategic plan goals ahead of time and had to rewrite the plan to keep it current and relevant.”

It’s important to be adaptable because nothing stays the same. “It’s more important to be agile and take advantage of opportunities that weren’t foreseen and make adjustments,” says Morris. “This and a continuous improvement mindset is the best way to exceed plan goals.”

- 11. Create a strategic planning team

As a business owner, you should never feel like you have to do everything alone.

A strategic planning team can help with every phase of the process, from creating a company vision to adapting your strategy week-to-week. Compose your team of key management staff and employees—some visionaries and some executors.

If you think you’re “too busy” for start strategic planning, then you need strategic planning more than you know. Having a focused plan allows you to focus your energies, so you’re working on your business, rather than in it. As a business owner, it is your responsibility to steer the ship, not put out day-to-day fires.

Yes, creating a strategic plan is challenging, and it’s certainly time-consuming, but it will make all the difference in achieving your long term goals. You’ll avoid making bad decisions and expending more effort than you need.

Try these 11 tips to get started, and then be flexible in your ongoing approach. You’ll be amazed at how much more streamlined your business processes will become when you are working with a long-term strategic plan.

Jodie Shaw is The Alternative Board (TAB)’s Chief Marketing Officer. She brings over 20 years of B2B marketing and 10 years in franchising to the role. Prior to to her work with TAB, Jodie served as the CEO and Global Chief Marketing Officer of an international business coaching franchise, serving more than 50 countries.

Table of Contents

Related Articles

6 Min. Read

7 Steps to Successful Project Planning

4 Min. Read

Strategy Is Useless Without Execution

5 Min. Read

How to Implement a Zero Waste Strategy for Your Business

8 Min. Read

How to Write a Business Proposal

The Bplans Newsletter

The Bplans Weekly

Subscribe now for weekly advice and free downloadable resources to help start and grow your business.

We care about your privacy. See our privacy policy .

The quickest way to turn a business idea into a business plan

Fill-in-the-blanks and automatic financials make it easy.

No thanks, I prefer writing 40-page documents.

Discover the world’s #1 plan building software

- Product overview

- All features

- App integrations

CAPABILITIES

- project icon Project management

- Project views

- Custom fields

- Status updates

- goal icon Goals and reporting

- Reporting dashboards

- workflow icon Workflows and automation

- portfolio icon Resource management

- Time tracking

- my-task icon Admin and security

- Admin console

- asana-intelligence icon Asana Intelligence

- list icon Personal

- premium icon Starter

- briefcase icon Advanced

- Goal management

- Organizational planning

- Campaign management

- Creative production

- Content calendars

- Marketing strategic planning

- Resource planning

- Project intake

- Product launches

- Employee onboarding

- View all uses arrow-right icon

- Project plans

- Team goals & objectives

- Team continuity

- Meeting agenda

- View all templates arrow-right icon

- Work management resources Discover best practices, watch webinars, get insights

- What's new Learn about the latest and greatest from Asana

- Customer stories See how the world's best organizations drive work innovation with Asana

- Help Center Get lots of tips, tricks, and advice to get the most from Asana

- Asana Academy Sign up for interactive courses and webinars to learn Asana

- Developers Learn more about building apps on the Asana platform

- Community programs Connect with and learn from Asana customers around the world

- Events Find out about upcoming events near you

- Partners Learn more about our partner programs

- Support Need help? Contact the Asana support team

- Asana for nonprofits Get more information on our nonprofit discount program, and apply.

Featured Reads

- Business strategy |

- What is strategic planning? A 5-step gu ...

What is strategic planning? A 5-step guide

Strategic planning is a process through which business leaders map out their vision for their organization’s growth and how they’re going to get there. In this article, we'll guide you through the strategic planning process, including why it's important, the benefits and best practices, and five steps to get you from beginning to end.